Your social media feed correct now is likely abuzz with statements that the FHFA’s new mortgage amount pricing changes (LLPAs) on regular mortgages favor potential buyers with negative credit over potential buyers with excellent credit score.

“A 620 FICO score receives a 1.75% charge lower price and a 740 FICO rating pays a 1% fee” reads one particular screenshot from a Fox News section creating the rounds on social.

Here’s the matter: which is not legitimate!

We’re likely to split down the FHFA’s most recent financial loan-amount pricing changes, most of which are by now in effect after currently being declared in January.

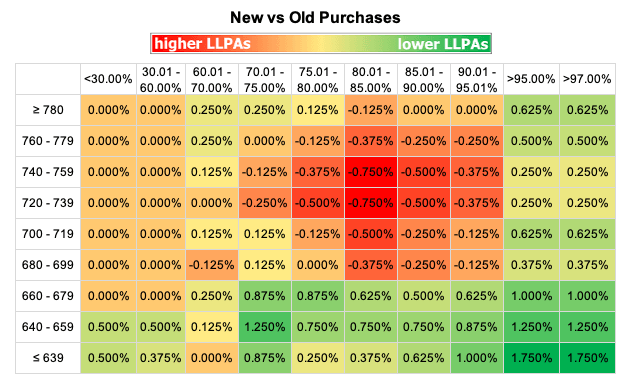

Let us start off with the fundamentals: The pricing grid includes credit bands that correspond with upfront expenses primarily based on the house loan product, financial loan-to-worth ratio, occupancy, etc. Here’s the latest design.

As you can see, the grid tops off at a 740 credit rating rating, meaning everyone with a FICO rating of 740 would shell out the identical fee on service fees as someone with a score of 780. Under the existing design, threat-dependent pricing (RBP) has been dependable. Commonly speaking, the reduced the credit rating score and increased the LTV, the better the upfront payment to mitigate the chance.

The new model tweaks the risk-based mostly pricing system in considerable strategies.

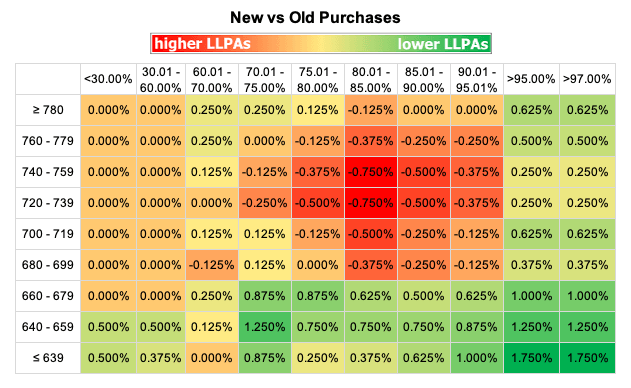

Here’s the new pricing matrix on purchase loans, which goes into result on Might 1 but basically talking has been in area for a lot more than a month. (This is not the grid the GSEs use, but it does demonstrate wherever modifications are. Key props to Matthew Graham of Mortgage loan News Each day for building this color-coded chart.)

There are new credit score bands beyond the 740. You will also recognize that the FHFA has enhanced fees on greater credit history scores and reduce LTVs. At the similar time, the FHFA has lowered expenses for debtors with decrease credit rating scores entire-prevent.

Let us get just one essential issue out of the way – FICO borrowers with lessen scores are not getting better fees than increased FICO debtors. If you have improved credit score, you are going to pay much less than another person with even worse credit rating. But there are some critical alterations that quantity to a cross-subsidy of types.

*Borrowers with credit score scores amongst 680 and 779 with down payments involving 10 and 20% will see a cost boost of among .13% and .75%.

*On the other side, to start with-time homebuyers with reduced or average residence income pay out no additional service fees in anyway, and debtors who put significantly less than 5% down across all FICO scores will gain.

*This chart does not show it, but shoppers who will see the biggest payment maximize are all those in search of a cash-out refinance, exactly where 60% of the populace analyzed by Experian would have expert higher costs with an common increase of 55 bps.

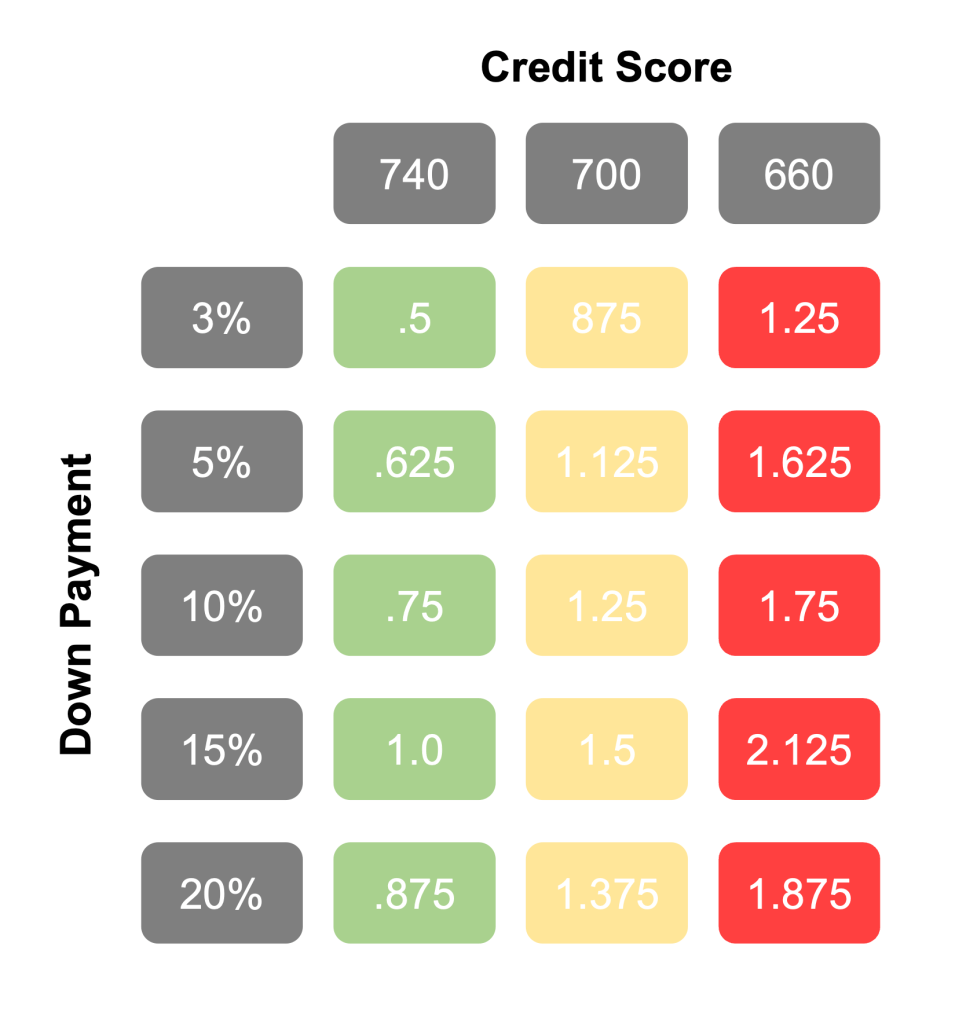

Rebecca Richardson, a personal loan officer at UMortgage, had a smart just take on the changes. Let us get a search at her example, in which the sales rate of the dwelling is $400,000 and the situations are credit rating scores of 740, 700 and 660, with corresponding down payments of 3%, 5%, 10%, 15% and 20%.

“People with good credit history are not receiving penalized, nor are they subsidizing reduced credit rating rating prospective buyers,” Richardson said in a LinkedIn article. “And which is generally for the reason that individuals who had been in the downpayment cheat code zone where by they were being putting extra than 15% down but fewer than 20% had their phrases sponsored by inexpensive mortgage loan insurance coverage procedures, which essentially gave them the exact phrases as any individual who was placing 25% down. To me these alterations are much more about bringing items in line wherever the real risk is primarily based off of downpayment.”

ALRIGHT, BUT WHY IS THE FHFA Executing THIS?

This pricing alter is in line with the Biden administration’s stated mission to supply housing funding opportunities to first-time homebuyers with reduced credit rating scores and those people in underserved communities.

There had been normally heading to be winners and losers when the FHFA decided to modify the pricing matrix. In this situation, a portion of fantastic-but-not-exceptional credit history debtors will obtain a little bit of a shock, a couple thousand bucks worthy of in some scenarios.

I imagine the FHFA is creating a calculation that far better-credit borrowers will nevertheless acquire the home inspite of an boost in upfront service fees and have plenty of skin in the recreation that possibility is not substantial. At the same time, a couple thousand pounds could be the change among a consumer with a reduced credit rating score obtaining homeownership or not.

Need to this plan transform come at the expense of these who are “doing points the ideal way,” as James Duncan, director of promoting at Prosper Property finance loan, put it? It is a reasonable question. This is a significant improve for the marketplace and environment a precedent on relocating absent from a pure hazard-based design is…a threat for the FHFA (even if the agency disagrees with that interpretation).

Everyone acknowledges that the GSEs need to be much better capitalized, but this coverage would look to harm center-class debtors and goal to benefit people who are extra possible to be in the FHA group. We’ll know really soon if this is a coverage failure.

What do you believe about it? Share your feelings with me and the techniques you are using to support buyers make the ideal option for their personal scenario.

DataDigest is a publication in which HW Media Running Editor James Kleimann breaks down the most significant stories in housing by a data lens. Indication up in this article! Have a issue in head? Electronic mail him at [email protected]