If you are the variety of homebuyer whose temper soars or plummets based on the most up-to-date mortgage loan costs, then this 7 days was a rough one particular.

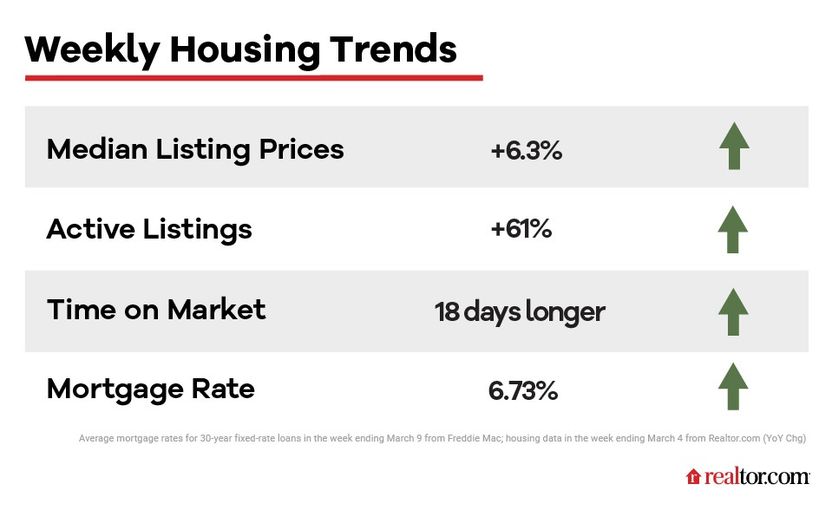

House loan fascination prices climbed to 6.73% for a 30-yr fastened-level mortgage loan, for the 7 days ending March 9, according to Freddie Mac. This implies today’s homebuyers will have to pay out practically 50% a lot more for every thirty day period for property than they would have just a calendar year previously.

This steep hike in housing prices may possibly hurt the rebound that experienced been emerging in the housing sector, when prices ended up lessen previously this calendar year.

“Recent symptoms of a housing bottom have been encouraging, but the still-shifting money and financial landscape helps make it hard to pinpoint irrespective of whether the floor is agency adequate to face up to these new difficulties,” says Realtor.com® Chief Economist Danielle Hale in her most recent analysis. “In the in the meantime, that suggests housing exercise is very likely to continue on roughly in line with its the latest reduced pace of product sales.”

As for what happens future, mortgage loan costs “will likely enjoy a solid function in determining no matter if the current market slows even further or picks up pace,” says Hale. “While the housing market place had revealed some symptoms of stabilizing, a renewed climb in mortgage charges could undermine the restoration.”

And although no one particular is aware for positive which way curiosity prices will head upcoming, stubborn inflation may well force the Fed to carry on bludgeoning the financial state with price hikes, which could mean mortgage costs may increase even further.

What then? We’ll explore what this all means for the two homebuyers and home sellers in our latest column of “How’s the Housing Current market This 7 days?”

How household costs react to high house loan costs

But there is a person shiny location for homebuyers: Housing rates may possibly continue to be growing, but that advancement is tapering off.

For the week ending March 4, dwelling selling prices improved by 6.3%, compared with where they were a calendar year earlier—the slowest increase noticed because June 2020, proper when the marketplace was recovering from the preliminary COVID-19 pandemic shock.

What is powering the slowing of property rate expansion? Believe that it or not, sellers have finally gotten the memo that purchasers need reduce rates to offset those increased desire costs they are spending currently. Despite quite a few sellers sitting out the latest industry, the ones who are making an attempt to locate a purchaser seem to be to be ultimately “calibrating their cost expectations,” according to Hale. As a result, price tag development is easing.

When home finance loan prices were being minimal but inching up in June 2022, potential buyers manufactured a previous dash to acquire a dwelling, which drove up residence rates to a file higher of $449,000. But by February 2023, as house loan charges had been pingponging involving 6% and 7%, listings settled toward a median inquiring price of $415,000.

And though listings took 18 much more times to sell—for the week ending March 4—than a yr previously, the speed is picking up a bit.

“This marks the 3rd week that the gap has shrunk, even as new listings continue being scarce, suggesting that buyers are active in the marketplace,” says Hale.

Residence stock proceeds to stagnate

When high property finance loan prices aren’t stopping particular prospective buyers, property sellers seem to be much more hesitant to jump in.

New listings have been falling for 35 weeks straight, plummeting by 26% for the week ending March 4, compared with a calendar year earlier. But in general household inventory (of both of those new and previous listings) carries on to balloon—up 61% from last year at this time.

This increase in the range of unsold houses on the marketplace may well seem shocking, right until the determine is regarded in a more substantial context that things in our pre-pandemic days.

“It’s critical to keep in mind that this calendar year-around-yr comparison is relative to early 2022, when active listings were being at or around prolonged-time period lows,” points out Hale. “So even right after this big year-more than-year attain, February details reveals that nationwide, there are only just additional than 50 percent as a lot of households for sale as were being out there pre-pandemic.”

50 percent as a lot of houses, for 50% more revenue? It is no speculate prospective buyers are hurting. Here’s hoping spring delivers far better news.