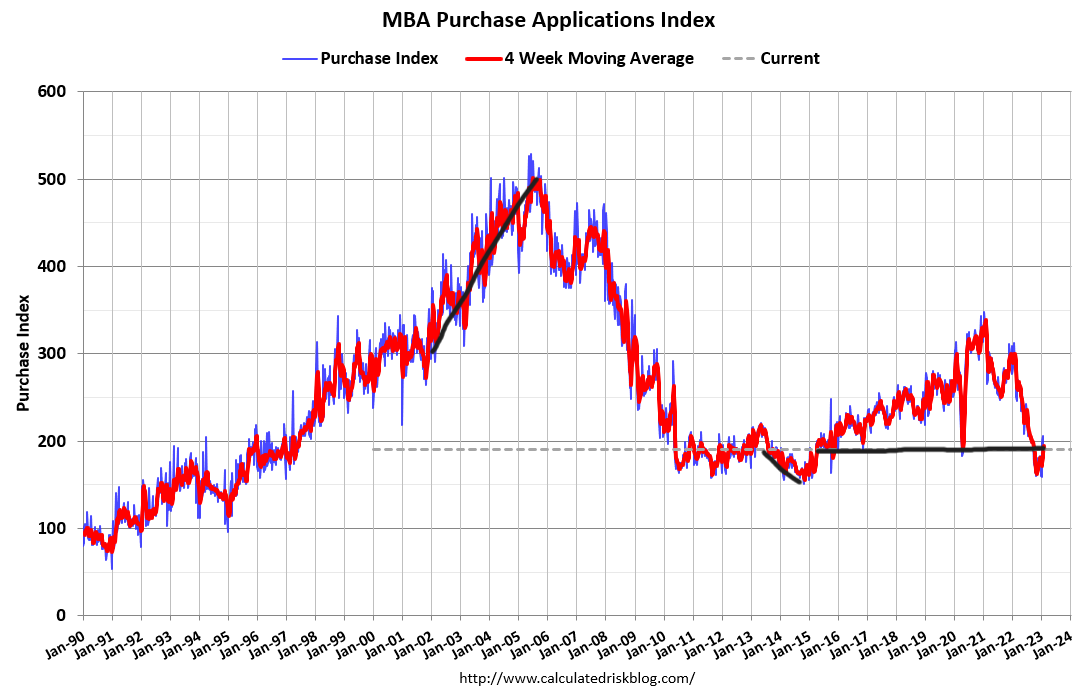

Very last yr, we had a historic dive in order software facts, but lately we identified a bottom and invest in applications have bounced from the lows. Due to the fact Nov. 9, when this knowledge line commenced to get better, and excluding the common severe slowdown the final and very first 7 days of the year, it is been optimistic exterior of 1 7 days. I am preserving an eye on how substantially progress we can get with home finance loan rates above 6%.

This 7 days, we will get a excellent exam with the order software details as home loan premiums have risen lately. I am wanting ahead to looking at how the info reacts to better fees. Unlike the COVID-19 restoration, which was quick and sharp, we are now working with a a lot diverse backdrop. Morgage premiums are larger and we’re operating from a great deal larger property costs as nicely.

The a person profit of the housing marketplace now is that times on the current market are no more time young adults, which implies we are getting nearer to a much more well balanced marketplace. This indicates purchasers have more say now in the household-buying course of action. Last but not least, all the constructive facts we have viewed given that Nov. 9 seems ahead 30-90 days, so the existing house gross sales will clearly show greater data coming up.

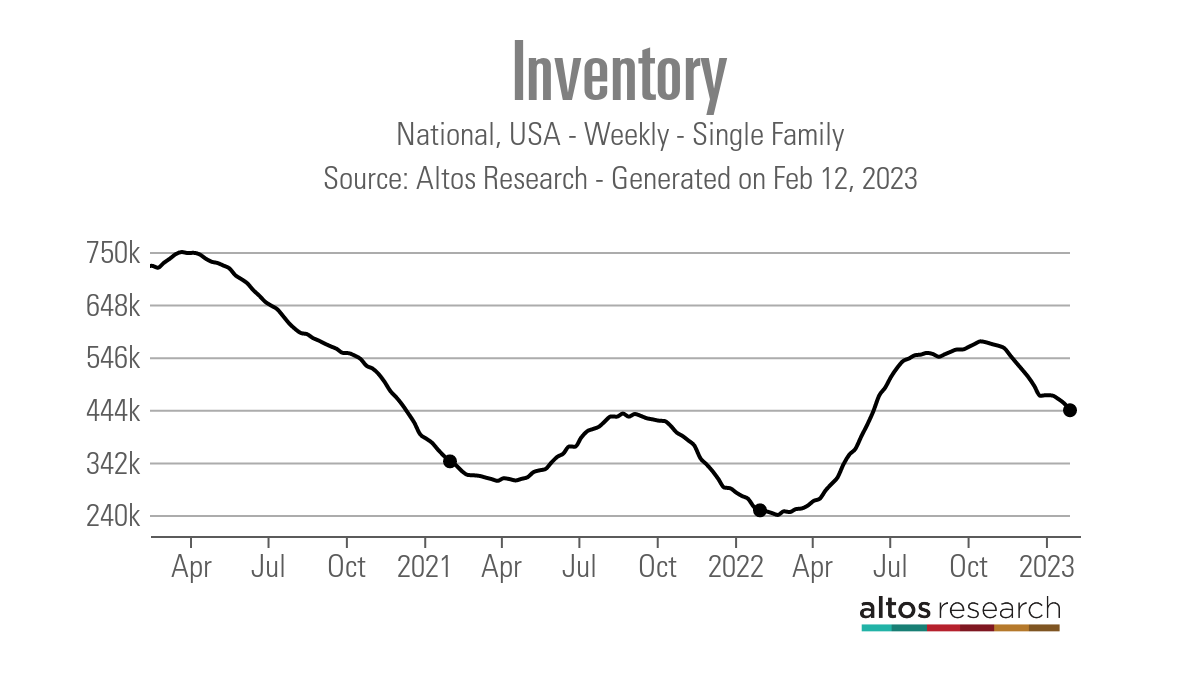

Weekly housing stock

When I noticed a slight improve in housing inventory in January, I bought incredibly excited for the reason that some of the need collapse we saw in the second 50 percent of 2022 was from people today deciding upon not to listing their homes for the reason that of their fear of acquiring a further. So, when I observed the slight stock raise, I assumed this was a superior pattern.

Ahead of 2020, weekly housing inventory bottomed out in the January/February timeframe, and then the seasonal spring maximize would start out. From 2014 to 2016, housing inventory bottomed out in January. From 2017 to 2019, the inventory stages in January and February have been very near to every other just before the seasonal push better.

Having said that, since 2020, this hasn’t been the circumstance — stock has tended to base out a minor afterwards in the year. In 2021, stock bottomed out in April, and in 2022 inventory bottomed out in March.

In the past two months, housing stock has been declining considerably and I hope we are coming closer to the bottom of the seasonal stock decrease. Regretably, previous week we saw a larger decrease in stock than the former week, as models fell by 13,238 according to Altos Exploration.

So I am crossing my fingers that we are getting closer to the stop of the seasonal inventory decline because the last factor we want to see is bidding wars once again, in particular with demand from customers operating from substantially lower degrees than what we observed in 2020/2021, and the early months of 2022. The beneficial part is that stock is however larger than past year

- Weekly stock adjust (Feb. 3-Feb. 10): Fell From 456,990 to 443,416

- Identical week previous 12 months (Feb. 4-Feb. 11): Fell from 255,662 to 249,161

Mainly because I could see that housing demographics have been likely to be very good in the several years 2020-2024, I actually didn’t want to see stock split to all-time lows all through this period of time. This reality produced my fear of household prices overheating, which they did, and once mortgage costs rose, the housing market place took an extreme affordability hit. Past 12 months, we had a historical dive in housing demand and didn’t get considerably inventory.

Unfortunately, we have a very good shot of the future current property income report exhibiting even reduce inventory degrees than the 970,000 level we are dealing with these days. This implies 2022 and 2023 are the only times in modern history in which the NAR active listing information is under 1 million.

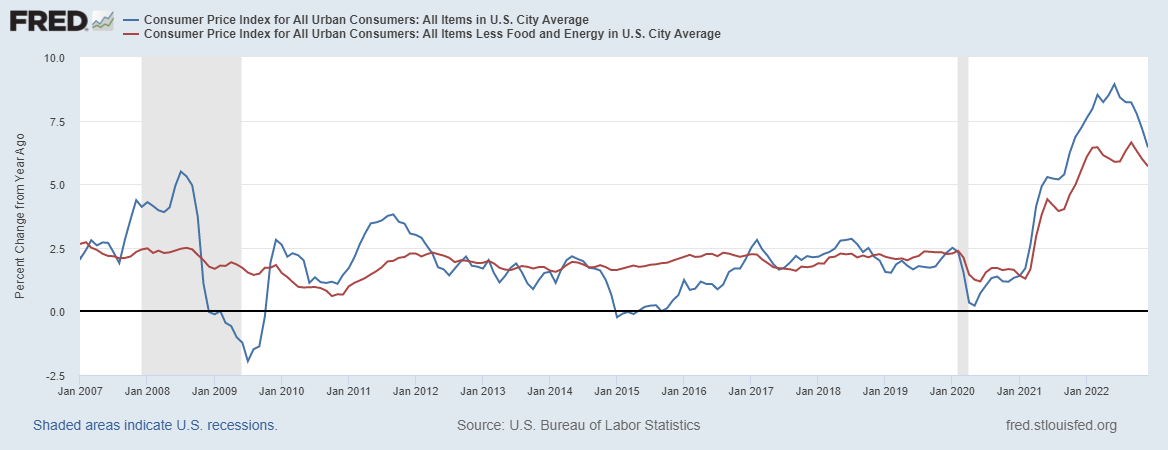

10-12 months yield and mortgage loan costs

In my 2023 forecast, if the economic system stayed agency my 10-12 months produce variety was concerning 3.21% and 4.25%, equating to mortgage loan fees being in a vary of 5.75% to 7.25%. For some time now, I have talked about how it would be challenging to crack underneath 3.42% with follow-through bond getting, this means property finance loan costs would slide more. The current market produced a several attempts to split that stage, but now bond yields have reversed higher.

The problem this 7 days with the CPI report details staying unveiled, is regardless of whether we will see a W forming in this chart, which would suggest bond yields head back again to 4.25%, or irrespective of whether the downtrend continues. Over time, the progress charge of inflation will interesting down as soon as rents get accounted for in a additional real-time manner.

Also, part of the 2023 forecast is that if the labor sector breaks, the 10-calendar year produce could get to 2.72%, which would imply mortgage rates in the reduced 5% range. And if the spreads get better, we could even have a 4-take care of on property finance loan premiums. For now, however, the labor marketplace is however sound.

The week forward

This will be an exciting week for economic details, bonds and housing. Initial and most important, this week’s buy application info is vital. It will be the initially applications facts amid a 50 percent a share go higher in house loan fees, and the following handful of months will be essential, also, if charges continue to be at 6.50% or head better. Remember, you must prioritize quantities about people today if the tracker knowledge goes adverse, you go with data instead than a personalized perception.

The major transfer for costs ought to be the Purchaser Price Index report this 7 days. If it’s hotter than expected, we could see bonds act negatively to that report. Also, this 7 days we have jobless claims, retail product sales, Producer Selling price Index inflation, the homebuilders’ self-assurance study, housing starts off and the Main Economic Index!

It is heading to be a busy week with financial facts that can go the bond marketplace and mortgage loan rates. One factor is specified from the data: house loan fees heading lower, even to just 5.99%, shifted the housing marketplace, which is a thing to try to remember as we go ahead