The housing market welcomed the news of lower mortgage rates last week after four reports showed that the labor market isn’t as tight as it seems and that the fear of 1970s-entrenched inflation was a lousy narrative. The 10-year yield finally broke below a critical technical level it had difficulty breaking for many months and we had a very small increase in inventory.

Here’s a quick rundown of the last week:

- Mortgage rates fell last week as the 10-year yield broke lower for the first time since the significant rise in rates last year.

- Active inventory rose by 823 single-family homes and new listing data is trending at all-time lows.

- Purchase applications fell 4% weekly, breaking a four-week streak of positive growth and are still down -35% year over year.

The 10-year yield and mortgage rates

An epic battle for the 10-year yield finally ended last week when it broke below the significant level of 3.42%-3.37% — the Gandalf line in the sand. After the jobs report on Friday, the bond yield retraced up to that critical line, but I tend not to put any weight on a holiday trading day. As you can see in the chart below, that red line was tough to break below, but it finally happened. This week’s trading in the bond market will be exciting with the upcoming inflation data.

In my 2023 forecast, I said that if the economy stays firm, the 10-year yield range should be between 3.21% and 4.25%, equating to 5.75% to 7.25% mortgage rates. If the economy gets weaker and we see a noticeable rise in jobless claims, the 10-year yield should go as low as 2.73%, translating to 5.25% mortgage rates.

This assumes the spreads between the 10-year yield and the 30-year stay wide, as the mortgage-backed securities market is still very stressed.

The banking crisis has put the entire year into a new variable spin as short-term rates now forecast rate cuts happening sooner than the Fed wants. However, everything looks right on the long end of the bond market, as jobless claims have been rising lately but not at my crucial level of 323,000 on the four-week moving average yet. If short term and long term rates keep falling with weaker economic data, it will force the Fed to cut rates faster than it originally wanted to.

The four-week moving average is running at 237,500, shown below on the chart.

Last Friday, I wrote about the jobs report and how it should be evident to anyone now, especially the Federal Reserve, that the fear of 1970s entrenched inflation was simply a joke. During the hottest labor market in history, wage growth was falling year-over-year, not spiraling out of control.

Mortgage rates started last week at 6.44% and fell to a low of 6.16%, then ended the week at 6.34%. So for all the drama we have had this year, the 10-year yield has held its range even with a national banking crisis. Now, we have enough data to see that the labor market isn’t as tight as it seems. With the CPI inflation data and retail sales this week, we could see another volatile pricing week, depending on the data.

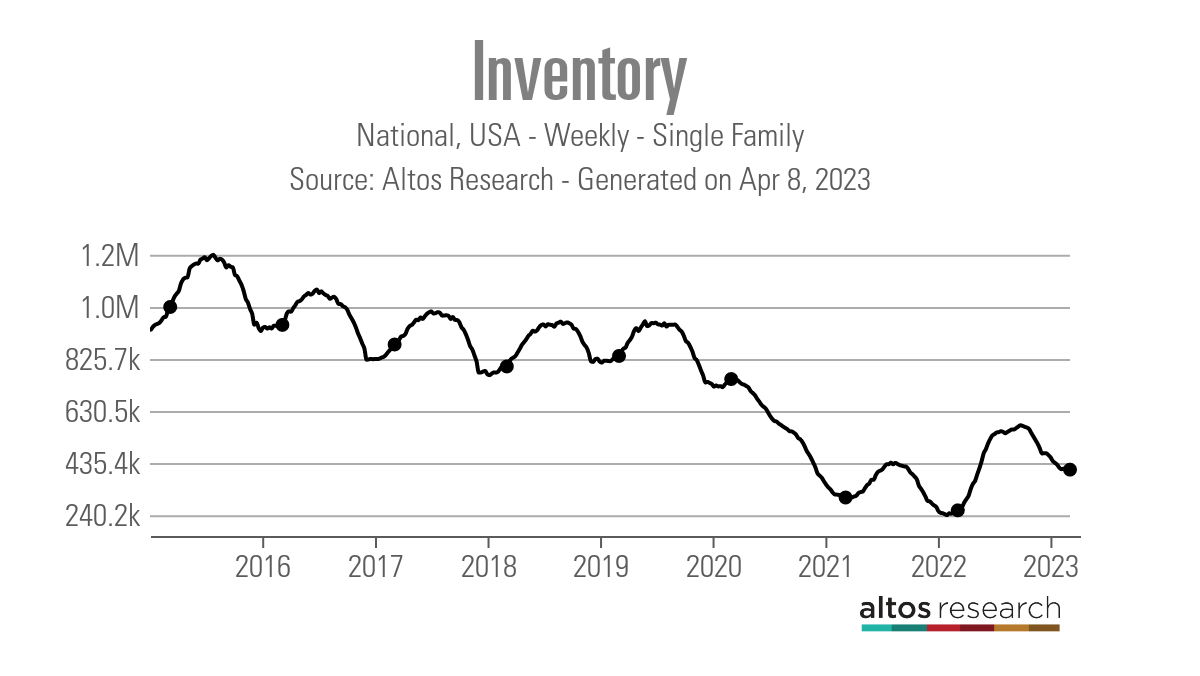

Weekly housing inventory

Looking at the Altos Research data from last week, the big question is: Have we seen the seasonal bottom in Inventory? I’m crossing my fingers that we may have finally reached the bottom. Housing inventory had only a tiny gain last week, but I am hopeful that April is the month we see the seasonal inventory increase.

- Weekly inventory change (March 31 – April 7): Inventory rose from 410,028 to 410,851

- Same week last year (April 1-April 8): Rose from 252,820 to 258,264

- The bottom for 2022 was 240,194

As you can see in the chart below, we are far from what a normal inventory channel looks like, and it’s been hard getting inventory back to pre-COVID-19 levels.

Mortgage rates in the previous economic expansion ranged between 3.25%-5%, and inventory had slowly been moving lower and lower. Last year we had the biggest mortgage rate spike in history, and it did create more inventory for us, but it couldn’t get us back to 2019 levels.

Last year, the weekly seasonal inventory bottom was set on March 4; we still need to confirm the weekly bottom in 2023. This year looks similar to 2021 data, which bottomed on April 9, so April could be the turning point.

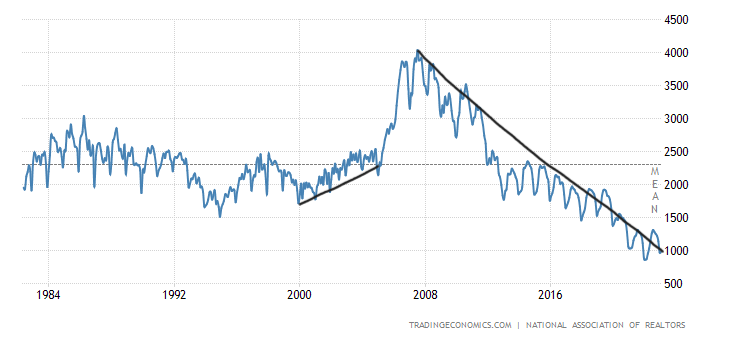

The NAR data going back decades shows how difficult it’s been to get back to anything normal on the active listing side. In 2007, when sales were down big, total active listings peaked at over 4 million. Today, even though sales were trending at 2007 levels, we are at 980,000 total active listings per the last existing home sales. Current housing Inventory is still not suitable for a healthy housing market.

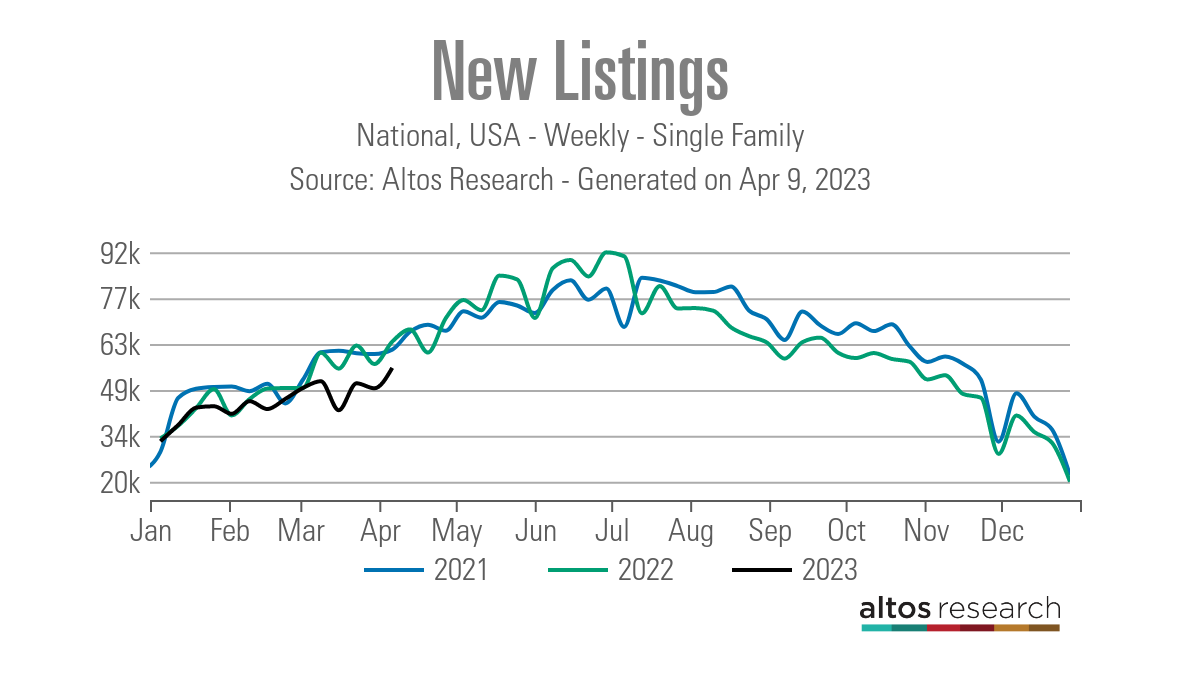

New listing data rose last week but is still trending at all-time lows in 2023. However, the fact that it is back on its seasonal growth trend is a good sign. The last thing the housing market needs is for new listing data to decline, so the growth we saw last week is a plus. I can’t stress enough how happy I was to see this data line.

Here are some weekly numbers to see the difference in new listings from past years over the same week. One thing to notice is that new listing data in 2022 was higher than in 2021. This isn’t the case, of course, this year, but if there is one data line I want to surpass 2022 levels, it is new listing data.

- 2021: 61,263

- 2022: 63,746

- 2023: 55,591

Compare weekly new listing data to previous years:

- 2015: 86,847

- 2016: 85,296

- 2017: 85,765

As you can see from the data above, homeowners aren’t rushing to sell out of panic since they’re in solid shape as the unemployment rate is still historically low. While U.S. households are employed and living a comfortable life with their low total housing cost, the last thing on their mind is giving up that comfort for the unknown.

We have natural sellers every year in the U.S., but now U.S. homeowners are sitting pretty with their low fixed debt cost. At the same time, their wages are growing faster than normal during an inflationary period. As you can see below, year-over-year wage growth is cooling down but still above what we saw in the previous decade.

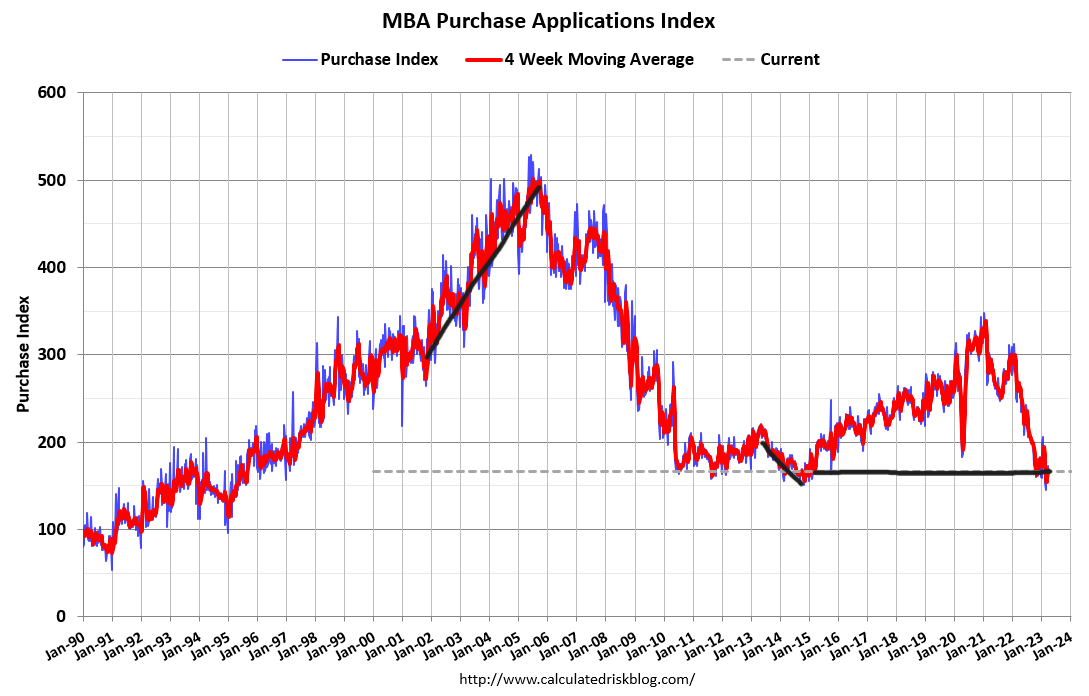

Purchase application data

Purchase application data has been one of the most improved housing market data lines since Nov. 9, 2022. This explains why the most recent existing home sales report had one of the most significant month-to-month sales prints ever. We have had three consecutive rising pending home sales reports as well.

Purchase application data fell 4% weekly in the last report, breaking a four-week positive streak. The index is down -35% year over year, which is a reminder that year-over-year comps will get easier, especially in the year’s second half. It will be interesting to see if lower mortgage rates will move the data much in the next report.

The purchase application data reports have been wild when mortgage rates have gone up or down. Traditionally, we wouldn’t have this volatility in this data line, but 2022 was a historic dive. When mortgage rates went from 5.99% to 7.10%, we had three negative prints, bringing this index to levels last seen in 1995.

However, as mortgage rates have fallen almost one percent from that 7.10% level, we have seen four out of the last five prints be positive. For 2023, looking at the data line during the vital seasonal period, we have had seven positive prints versus five negative prints.

Remember, this data line looks out 30-90 days before it hits the sales data. Also, the seasonality of this data line is almost over. I typically put more weight on this data line from the second week of January to the first week of May since total volumes traditionally fall after May.

The week ahead for inflation and mortgage rates

It’s inflation week with two inflation reports. The first is the all-important CPI report, which will show that the lower year-over-year trend in inflation data continues this week. Last September when the CPI report was coming out, CNBC asked me to talk about inflation data, and my take was that we would have a positive story in 2023 as the growth rate of rent inflation will fade.

This is important because without rent inflation booming, it’s hard for inflation levels to stay high. It’s better for mortgage rates when rent inflation slows down as it will take the growth rate if inflation down with it, and mortgage rates head higher when the growth rate of inflation falls. This is happening this year; the year-over-year inflation growth rate is falling and will fall more in the following report. Read about why mortgage rates aren’t higher here.

Of course, now it’s well known that shelter inflation on the CPI report lags badly, so the numbers we see this week are still not reality.

This week we also have the Producer Price Index inflation report and we will have retail sales on Friday. Now retail sales are going to be interesting because some of the credit growth that we have seen — which keeps the economy expanding — has cooled a tad, so it will be an excellent test to see if we see some slowing down in retail sales.

And of course, all eyes are on the bond market. As I recently talked about on CNBC, the U.S. housing market revolves around the 10-year yield and what drives that up and down. We shall see how the economic data impacts the bond market and mortgage rates. With the Gandalf line breaking and the labor market starting to show some softening, every report will be more and more critical.