Not only has the knowledge stayed organization, but the economic facts has enhanced not too long ago.

Also, fuel price ranges are down from the peak, and the inflation progress rate is no for a longer period skyrocketing. If the labor market breaks this 12 months, meaning jobless claims noticeably rise, that must deliver the 10-calendar year generate to 2.73%, and home loan premiums can go as very low as 5.25%.

Jobless promises have been strong for some time, and this is a big motive why I really do not believe the Federal Reserve is heading to pivot exterior of this. They generally built it distinct they want the labor marketplace to crack, so go with that premise until eventually they say otherwise.

Housing permits will slide all yr, but profits picked up just lately, a positive for the economic climate, which means additional transfers of commissions. An improving overall economy places a lot more possibility to the upside in costs and bond yields, in particular if inflation facts picks up.

If the reverse was going on, financial information would get weaker with a lot less consumption and far more individuals submitting for unemployment statements. Rates should really fall due to the fact, compared with in the 1970s, decrease financial advancement and much less jobs must not develop extra inflation as it did in 1974.

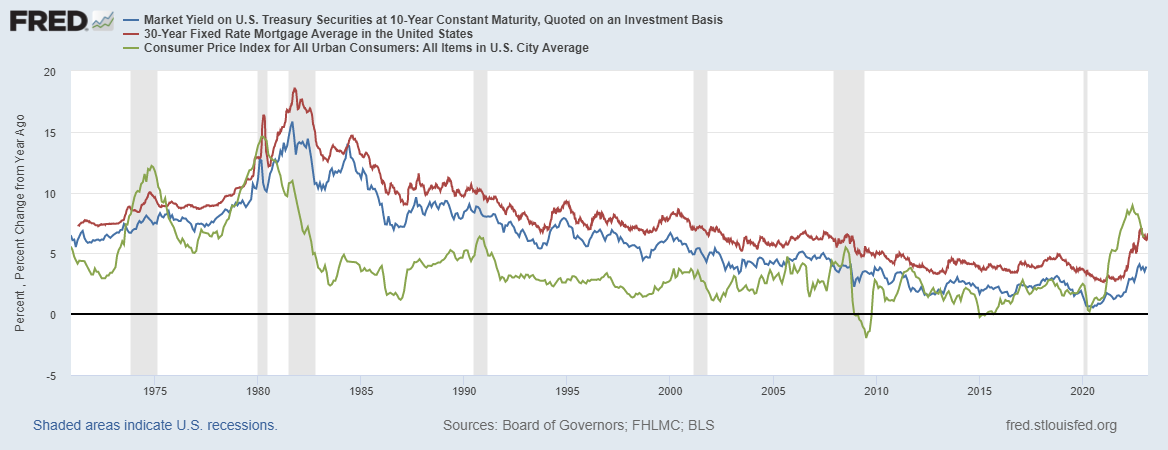

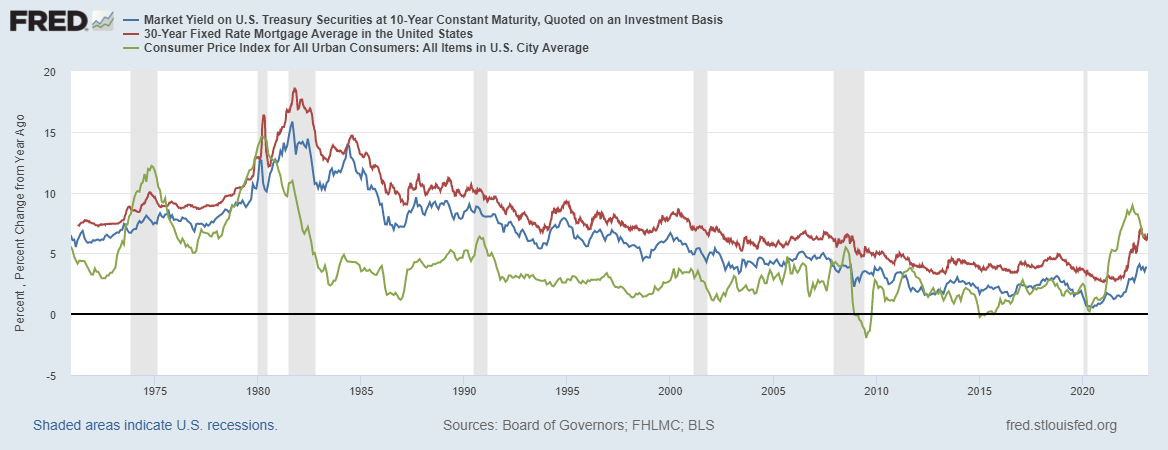

It is real that inflation is booming like we have not viewed considering that the 1970s, but the reality is that if the bond sector thought in entrenched inflation, it would have been pricing the 10-calendar year generate considerably increased over the past calendar year.

CPI inflation took off a several times in the 1970s, along with mortgage premiums and the 10-year yield. Now inflation has taken off yet again, but mortgage fees have still to get higher than 8% as we saw in the mid to late 1970s, and the bond market place has also not damaged above 5.25% on the 10-yr generate. Also, the Federal Reserve isn’t discussing having the Fed Cash charge again to late 1970 ranges both.

Housing in the 1970s was booming!

Have you ever wondered why the Federal Reserve explained we necessary a housing reset in March 2022 but not a labor market place reset? They’re focusing on the labor sector in the sense that if extra People shed their work opportunities, we will have extra supply of staff, which will direct to fewer wage development and considerably less inflation. On the other hand, they did not use the word reset concerning the labor market place.

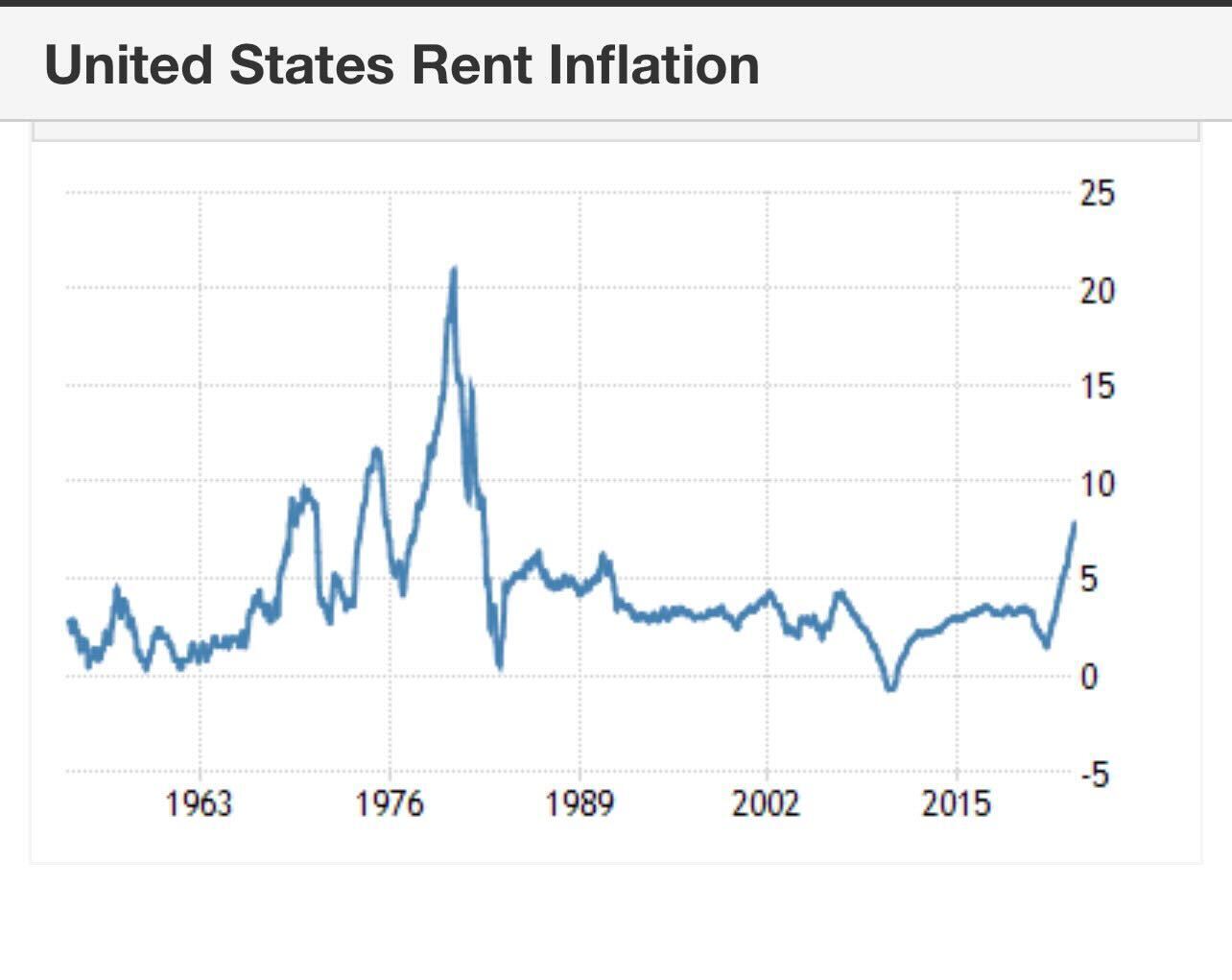

The Federal Reserve said it doesn’t want the 1970s entrenched inflation. This indicates if you are to feel them, they are afraid to dying of a housing growth! In the 1970s, we noticed a few renting inflation booms, but the entrenched inflation in the mid to late 1970s is what they really don’t want to see once more.

Even with the economic downturn in 1974, inflation and prices grew, and in the late 1970s inflation and housing need ended up booming larger. I do not consider they believe that in this variety of inflation, so they’re conversing about receiving nearer to the conclusion of their amount hikes.

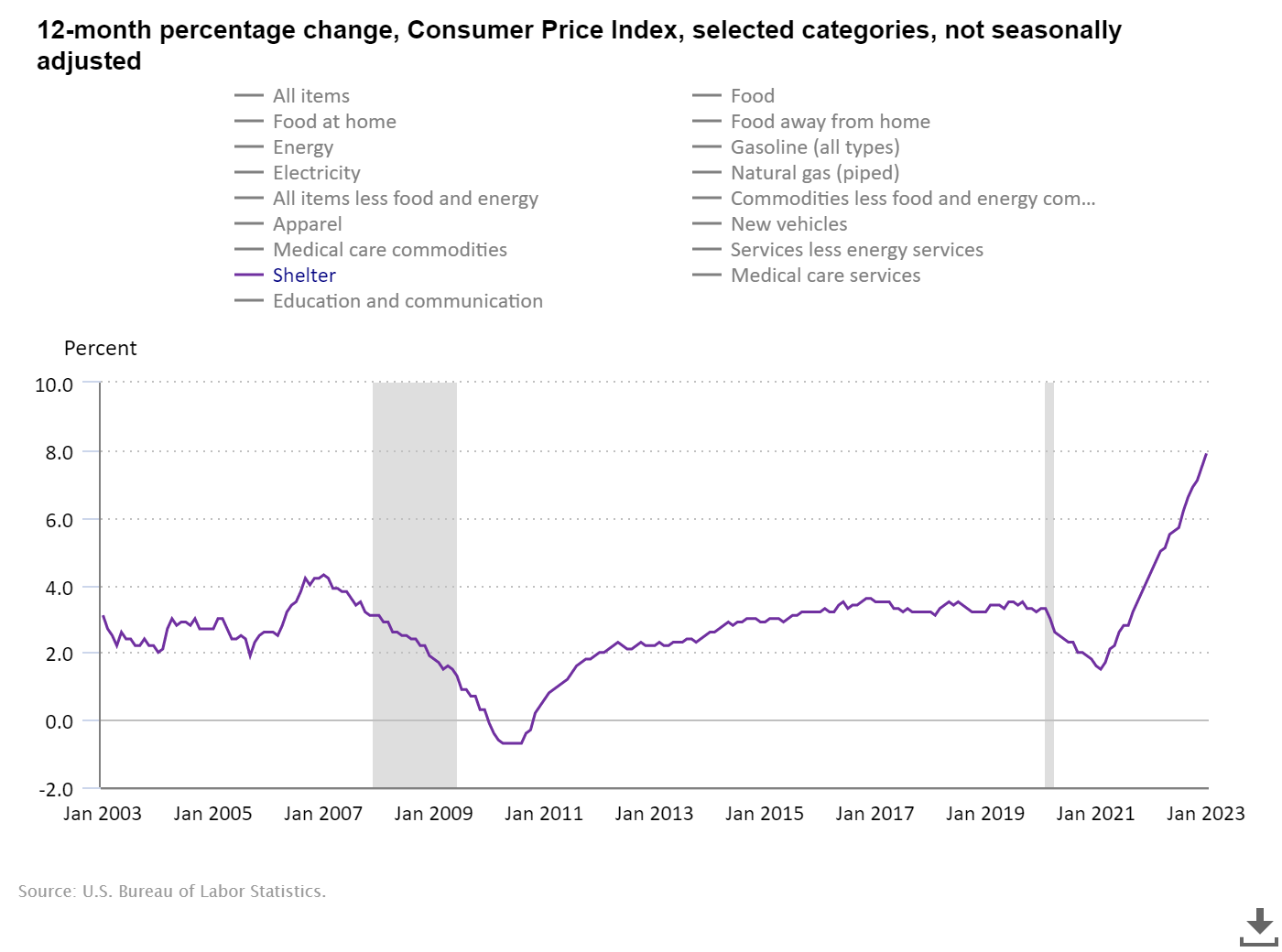

Considering that 43% of core CPI is shelter inflation, you can see why rents are so critical. After the 1970s, the growth fee of inflation cooled off as rent inflation cooled off and was very steady up until eventually the world wide pandemic, as you can see beneath, the year-around-yr inflation growth level.

It’s well regarded now that the CPI rent inflation information lags terribly, and we are presently seeing the progress charge of rent cooldown, some thing I talked about on CNBC final September on CPI inflation working day.

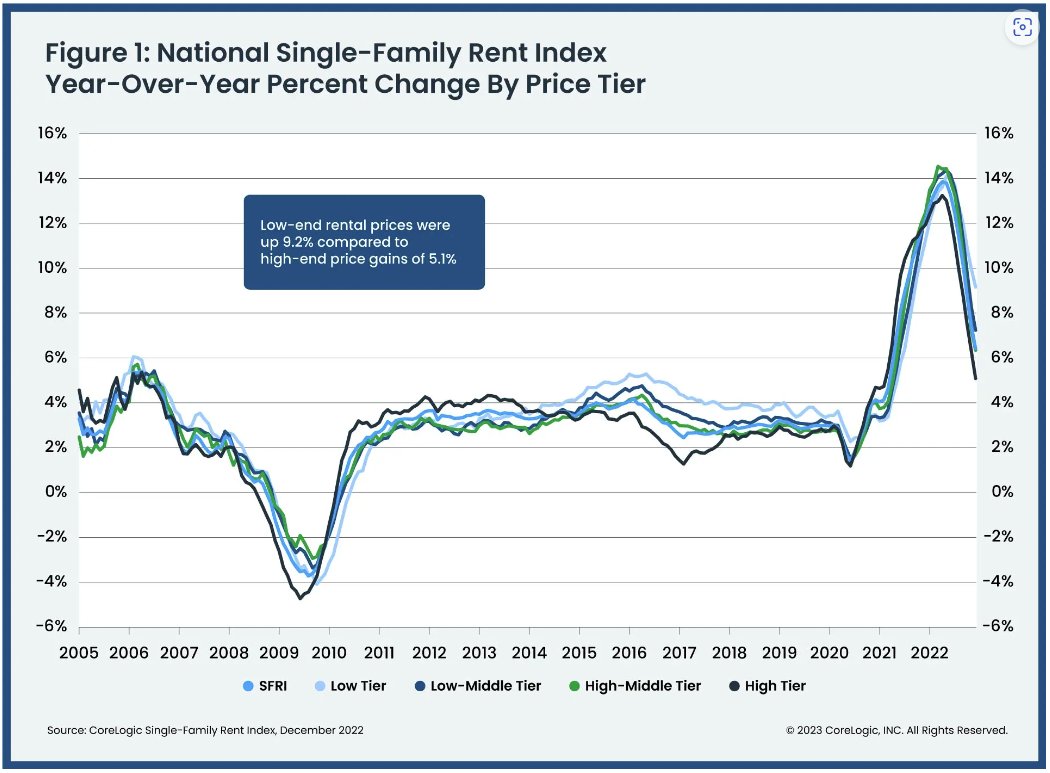

From CoreLogic:

Now search at the shelter inflation details of CPI nowadays huge difference. To the Fed’s credit, they did build an inflation index to get shelter inflation away from the conversation, indicating they want to emphasis extra on assistance inflation because of to the lag in rent inflation.

Once again, this is why I think they’re worried of 1970s inflation, but they also know deep down inside, as the bond sector knows, we never have the backdrop of 1970s inflation. I was not sure if they realized of the lag factor for a while there, but they fixed this by creating their index in December that it does not count housing inflation.

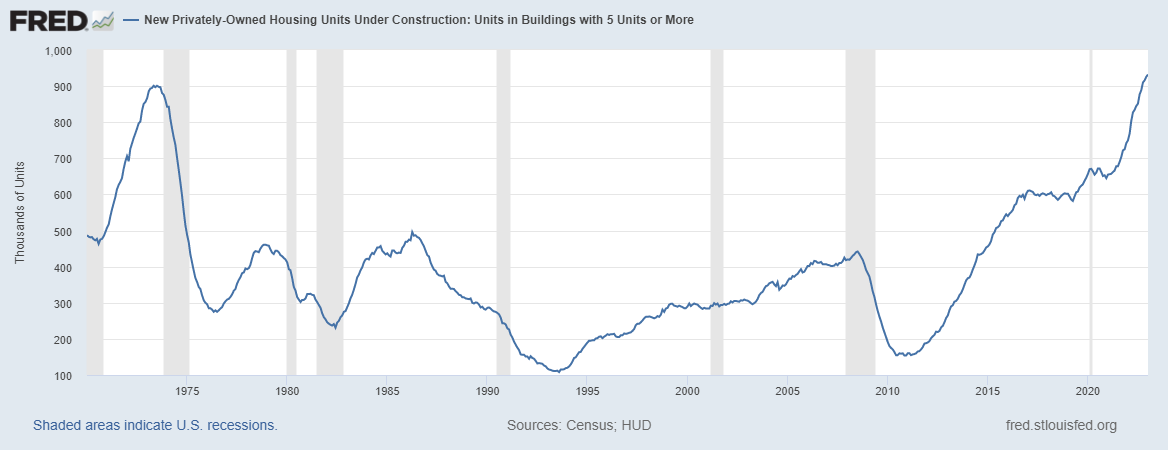

We have a record amount of 5-unit construction heading on, so the most important element of CPI is by now slipping in true terms. We have a very good provide coming on the internet, way too, with the Fed accomplishing what it can to neat the financial state down.

So the outlook is good in this article on protecting against a 1970s inflationary growth on rent development. As we can see under, the 1974 recession also killed the advancement of 5 models under construction. This is not the situation right now!

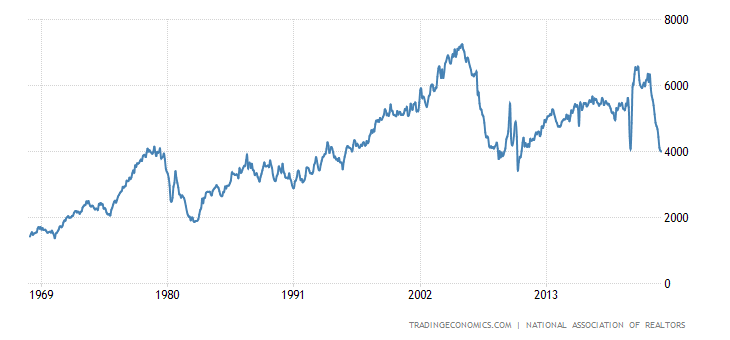

I have discovered recently that persons do not know how substantially housing boomed back again in the mid to late 1970s. Present property sales doubled prior to we observed the collapse in demand from customers. We went from 2 million to 4 million and back again to 2 million. We are not in the growth product sales demand from customers phase these days as existing home income experienced the major a person-calendar year every month profits collapse.

So, whilst I am not a Fed pivot human being until eventually jobless claims split in excess of 323,000 on the 4-week shifting normal, I did have the peak 10-yr produce at 4.25% this calendar year with a 7.25% peak mortgage loan price stage. I am not blinded to the fact that inflation and expansion have restrictions as premiums increase, with the offer of five-unit coming on line.

I believe the bond sector has constantly identified this, which is why the higher inflation ranges, the 10-12 months yield, and mortgage loan prices really don’t seem like the 1970s currently.

Why would it be considerably less very likely for home loan charges to increase from these ranges compared to why they would be a lot more probable to tumble?

The progress level of inflation is by now cooling off, source chains are getting greater, rental inflation will ultimately catch up into the inflation facts, plus we have far more supply of rental units coming on line. All these points place to us not getting a 1970s redux.

It’s finding from below to there that will have a large amount of financial sounds and confusion, and the Fed doesn’t do itself any favors when they discuss weekly and sound like they are perplexed about what to do.

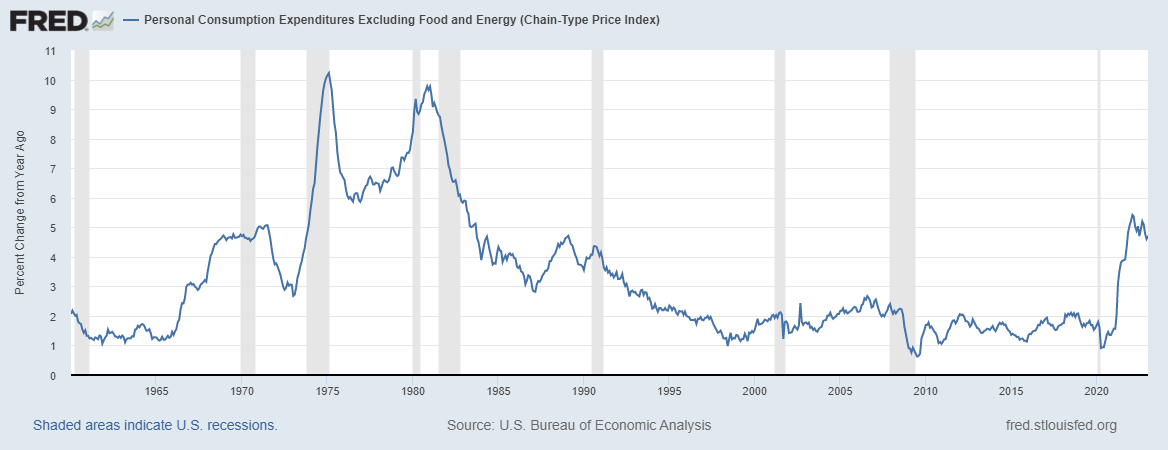

However, with that claimed, we need to have a a few-cope with on the Main PCE development rate of inflation by the finish of the year. Again in the 1970s, this data line which is the Fed’s principal target degree, was nearing 10%. Right now it is at 4.7% and even the Fed’s forecast exhibits this slowing down by the finish of the year.

Although we are not going to strike the Fed’s focus on of 2% 12 months-over-12 months expansion on inflation this 12 months, the progress charge of main PCE is slowing down now, which shows why the Fed and the bond marketplace do not think we are heading to get to 1970s-level inflation.

We have a great deal of sounds about fees and inflation recently, and some people today say that to demolish inflation, we want a more robust-than-expected occupation loss recession, these kinds of as we observed in the 1970s. Ideally, the data I confirmed you now can place the 1970s to rest.

If your child boomer buddies are frightened of the 1970s yet again, give them a hug and notify them everything will be okay we will endure this. Do not overlook that Fed level hikes have a lag, simply because they have a lagging affect to the financial system, the Fed really desires to stop climbing before long, so they don’t have to slash fees faster than they want.