When prospective consumers operate in really regulated economic markets, business revenue don’t come easy. Blend co-founder and CEO Nima Ghamsari appreciates this potentially improved than any individual.

It wasn’t until finally 2014 – two yrs just after his cloud banking system launched – that Movement Home finance loan took the leap and digitized its home finance loan origination and underwriting process with Blend’s tech stack. It was the initial big loan company to do so, according to Ghamsari.

“The tricky matter about doing the job with banking companies is they not only will need a product and a remedy that’s much better, they really do not want to be initially movers, and they only want to go if there is a catalyst,” Ghamsari reflected all through a fireplace chat with Plaid CEO Zach Perret past yr. “I try to remember that 2012, 2013, 2014 have been seriously hard yrs for us due to the fact the product is actually good, it was early and there were no proof points, they didn’t want to be the very first mover simply because if it did not get the job done out the individual who hired us was likely to shed their task. And there was no catalyst.”

That catalyst finished up getting Rocket Home finance loan’s “Push button, get mortgage” campaign in 2015. Out of the blue it clicked for financial institution executives, Ghamsari stated. Rocket would take in their lunch if they did not get rid of the inefficient, paper-weighty design.

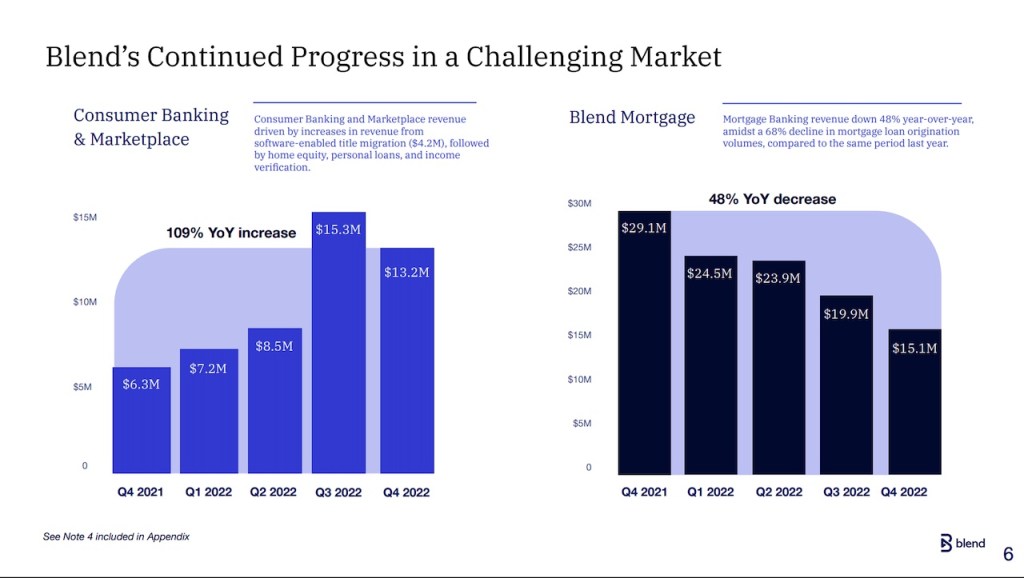

In the ensuing yrs, Mix brought on hundreds of purchasers, such as Wells Fargo, To start with Republic Lender, Mr. Cooper and U.S. Financial institution. When the home finance loan marketplace produced much more than $8.5 trillion in origination quantity in 2020 and 2021 and posted history revenue, it was Blend’s electronic technology that driven about a quarter of people mortgages.

Blend’s customers could originate a home loan a 7 days quicker with Blend’s technological innovation, and they saved hundreds of dollars for every loan in operations expenditures. The platform seamlessly built-in with CoreLogic for credit rating scores, Plaid for lender account details, Google Maps for place details, as very well as preferred home finance loan programs from Black Knight, ICE Mortgage Engineering and many others.

Ghamsari, a Stanford grad and former skilled poker player who normally reported he appreciated to guess on himself, rang the opening bell on Wall Street on July 16, 2021. His business was valued at $4 billion even even though it experienced under no circumstances right before turned a profit.

The IPO gave Mix $360 million, the funds required to increase marketplace share, develop new solutions and dive further into new sectors inside of fintech — including consumer banking items.

It was intelligent to diversify from a property finance loan field infamous for its growth-and-bust cyclicality. But just about two several years after heading community, with its home finance loan-major client base reeling from the Federal Reserve’s unprecedented collection of interest rate hikes, Blend’s losses have ballooned to over $1 billion.

Ghamsari is now faced with a acquainted dilemma: he needs to encourage the marketplace that Blend’s latest evolution—to a platform-as-a-company company—will transform purchaser banking, just as it did mortgage a couple decades ago. He’ll also have to do it in advance of the dollars operates out: As of Monday, April 3, Blend’s inventory is buying and selling at 99 cents a share, its market cap has nosedived to $239 million, the company’s personal debt load is large relative to its worth, and the runway is shrinking.

Blend’s developing blocks

When Mix has been increasing into the buyer lending place due to the fact 2019, the the greater part of its profits remains tied to the home loan enterprise.

And Blend’s intention to develop into a system-as-a-provider business is nevertheless in its early phases, analysts and market observers said in an interview with HousingWire. The firm’s survivability, allow on your own profitability, will count on rightsizing the enterprise and accelerating its diversification, analysts and observers stated.

In March, Mix released what it known as a “composable tech” platform, recognized internally as “Blend Builder.” Customers can develop their have origination solutions and leverage integrations with modular blocks. These blocks cover the full end-to-close origination approach, which includes pricing, money verification and closing, as nicely as an orchestration layer that enables creditors to develop custom made workflows in a very low-code, drag-and-drop ecosystem. Blend provides pre-developed answers, which includes prompt household equity, deposit accounts and credit score playing cards. These goods are ready to use, with integration templates readily available that let for brief deployment, executives noted.

We are setting up a path in the direction of profitability, even if we do not see a substantial macro advancement.

Amir Jafari, Blend’s head of Finance and Administration

“Mortgage financial loans stay an important phase for us. On the other hand, as we create out our Blend Builder Platform and migrate current customers–or indicator new ones–to our customer banking suite, we will be setting up a countercyclical buffer for moments like these, when growing our in general whole addressable sector,” Amir Jafari, head of finance and administration, explained in an emailed response to HousingWire.

“We are setting up a path towards profitability, even if we do not see a sizeable macro enhancement,”Jafari mentioned.

(The firm did not make executives accessible for an interview with HousingWire.)

Blend’s evolution into a platform firm will let the agency to be far more scalable in excess of the long operate, as opposed to staying squarely concentrated on the home loan classification, in accordance to Ryan Tomasello, controlling director at Keefe, Bruyette & Woods (KBW).

“But it all comes down to execution,” Tomasello reported. “The management’s concentration on diversifying the company into other locations like customer banking is supposed to permit the company’s outlook to not be as tied to home finance loan but the present combine of the organization is nevertheless very indexed to property finance loan volumes.”

“I feel Mix is in all probability an acquisition concentrate on additional than anything at all,” Tammy Richards, CEO of mortgage loan consulting agency Lendarch, claimed, noting that Mix experienced $796 million in losses in 2022. “I also consider that no firm can sustain these types of losses and be in a position to survive.”

The system pivot

The firm’s pivot to the Blend Builder platform came as the mortgage lending environment actually turned sour, a previous personnel instructed HousingWire.

“Blend was conversing about a pivot to the Blend Builder platform in the summer months. Setting up [in] the fourth quarter—when the 3rd round of layoffs happened—was when workers realized how a lot of a pivot was remaining designed,” reported the previous worker, who asked for anonymity.

By the time a fourth round of layoffs was declared in January 2023, a major amount of means experienced been reallocated to Mix Builder, the previous personnel explained.

The cumulative layoffs at Mix have resulted in significant operational changes. About the third or fourth quarter of 2022, mortgage creditors ended up reassigned to standard portfolios rather of possessing devoted associates on the profits and account servicing staff, the previous employee claimed.

“As we declared earlier this 12 months, we’ve allotted an increased part of working costs into Blend Builder as component of our evolution into a platform business,” a Blend spokesperson claimed in response. “That and other initiatives supporting our path to profitability incorporate many operational realignments, but through it, our motivation to giving our greatest attainable provider to our house loan customers has not transformed.”

The all round prospective of the platform is enormous, observers reported.

Blend Builder is the type of option that the premier-sized banking institutions are looking for proper now — a balance in between buying main-edge 3rd-celebration software program put together with a program framework that is remarkably customizable, an crucial attribute for larger sized banking institutions, Joseph Vafi, an analyst at Canaccord Genuity, wrote in a investigate notice.

“People are normally seeking to enhance their tech approach and it just can make a simplified way of getting ready to do that,” Richards included.

For independent house loan financial institutions that really don’t have significant progress groups to be ready to establish factors to link to Blend, the Builder platform will be specially beneficial, Richards defined.

But regardless of whether Mix can develop into the go-to system for mortgage and purchaser banking in the next number of many years will rely seriously on the company slicing its money losses.

Coming debts and a shrinking runway

Even if the Mix Builder Platform receives off to a incredibly hot get started, the firm has a slew of fiscal worries to get over.

For starters, its bread-and-butter house loan shoppers on average are originating fewer than 50 % the volume they did a yr back. That signifies considerably less income for Mix, whose revenue design is tied to customer volume.

More urgent is climbing expenses. Running costs in 2022 jumped to $835.8 million from $313.2 million in 2021, with $450 million similar to the Title 365 acquisition from Mr. Cooper.

To compound that, Mr. Cooper can drive Blend to buy its remaining 9.9% possession desire with a place alternative, which was valued in December 2022 at $53.2 million.

Mix also has a $225 million time period financial loan that will come due in 2025.

I think Mix is in all probability an acquisition goal a lot more than something. I also think that no corporation can sustain individuals kinds of losses and be in a position to endure.

Tammy Richards, Head of Property finance loan Consultancy Lendarch

Whilst the organization has funds, income equivalents and marketable securities totaling $354.1 million, Mix incurred an running cash melt away of $190.42 million in 2022. (Cash burn for the fourth quarter came down to about $47.3 million.)

“So when you imagine about the runway, that indicates, just based on the fourth quarter reduction, that indicates, significantly less than two decades of runway. That’s if it’s implicitly solely this quarter, and not providing the company credit rating for losses that ought to narrow as a result of this yr, as they see the profit of specified value framework steps that they’ve taken,” Tomasello observed.

Even though Blend touted new small business associations in its Builder platform with shoppers like Credit history Just one Financial institution and Compeer Economical in the fourth quarter, Blend does not hope to article a earnings in the to start with quarter of 2023. It has projected non-GAAP losses of among $37 million and $39 million.

“Continued house loan and total lending marketplace volatility impacts our visibility into the earnings restoration. Even so, we established our lengthier term path to profitability with an prolonged downturn in line,” Jafari stated.

What is future for Blend?

As of the 1st quarter, Mix will re-phase revenues into its purchaser suite and the relaxation of the company in the home finance loan sector, which will provide a far better feeling of how Blend is progressing into a system corporation, Tomasello reported.

Mix will involve all of its client banking products and solutions — such as deposits, residence equity, credit history playing cards, personal financial loans, and platform subscription access — in a one consumer suite lineup.

For its house loan enterprise, the organization will consolidate revenues from its marketplaces and incorporate-on merchandise, like revenue and close, into a solitary mortgage loan suite lineup, which reflects its concentration on increasing associations with home loan buyers.

“It’s really hard to parse as a result of how profitable they are in their purchaser banking expansion based mostly on how they now current their financials and section their revenues (…) It (shopper banking and market) does include items like e-near options on the house loan facet or money verification and also their software package and title enterprise,” Tomasello mentioned.

Blend started charging a recurring system charge in addition to the current “success-based” transaction payment in the fourth quarter that will crank out typical recurring profits for all purchaser banking deals.

Blend expects to return to sequential advancement in the 1st quarter and each subsequent quarter in 2023.

“Our precedence this year is to far better serve our customers’ needs as they alter, by growing and deepening our interactions with them by means of flexible goods that most effective fulfill their needs at any provided place in time,” Jafari instructed HousingWire.

Jafari mentioned that growing the home finance loan banking business and growing the person base for Mix Builder are not mutually special and can the two be attained if Blend carries on to construct the very best goods on the marketplace.

Of class, the best products does not normally gain. Time and cash appear into play.

“I consider they are at the commencing of their journey,” Richards reported. “A whole lot of businesses are attempting to be like an Amazon for home finance loan banking so that a purchaser has a 1-prevent store for dwelling acquiring or house advertising experience…They’re likely to have to be intelligent with their investments into the tech stack seeking to the foreseeable future to make positive they are conference long term requirements simply because the business is really hunting for efficiencies and value personal savings.”