Last June, the Federal Reserve claimed it preferred a housing reset, which meant it needed better home loan charges to destroy the housing industry. This facilitated the largest decline in existing home income for a solitary 12 months that we will at any time see in present day-working day historical past thanks to the superior degree of revenue in January of 2022.

Now, the Federal Reserve realized its key purpose the times on the marketplace are now previously mentioned 30 times, which was the most significant information line to get housing again to somewhat normal. Of study course, this place the housing sector into a recession on June 16, 2022.

Right now I am a joyful camper due to the fact last yr, the housing market place was savagely harmful with days on the industry in the teenagers, and now we are back to a normal stage around 30 days. We just cannot have a performing housing market place with days on the sector down below 20 days.

Two awful factors could make clear why the times on the market place are below 20 times. No. 1, a large credit history housing bubble in demand, which will pop eventually. Of course, we really do not have that now. However, the next is that stock is merely too low, with as well quite a few men and women chasing also number of households, which usually means much too numerous bidding wars. We are not acquiring bidding wars like we noticed when the days on the market place have been below 20 days.

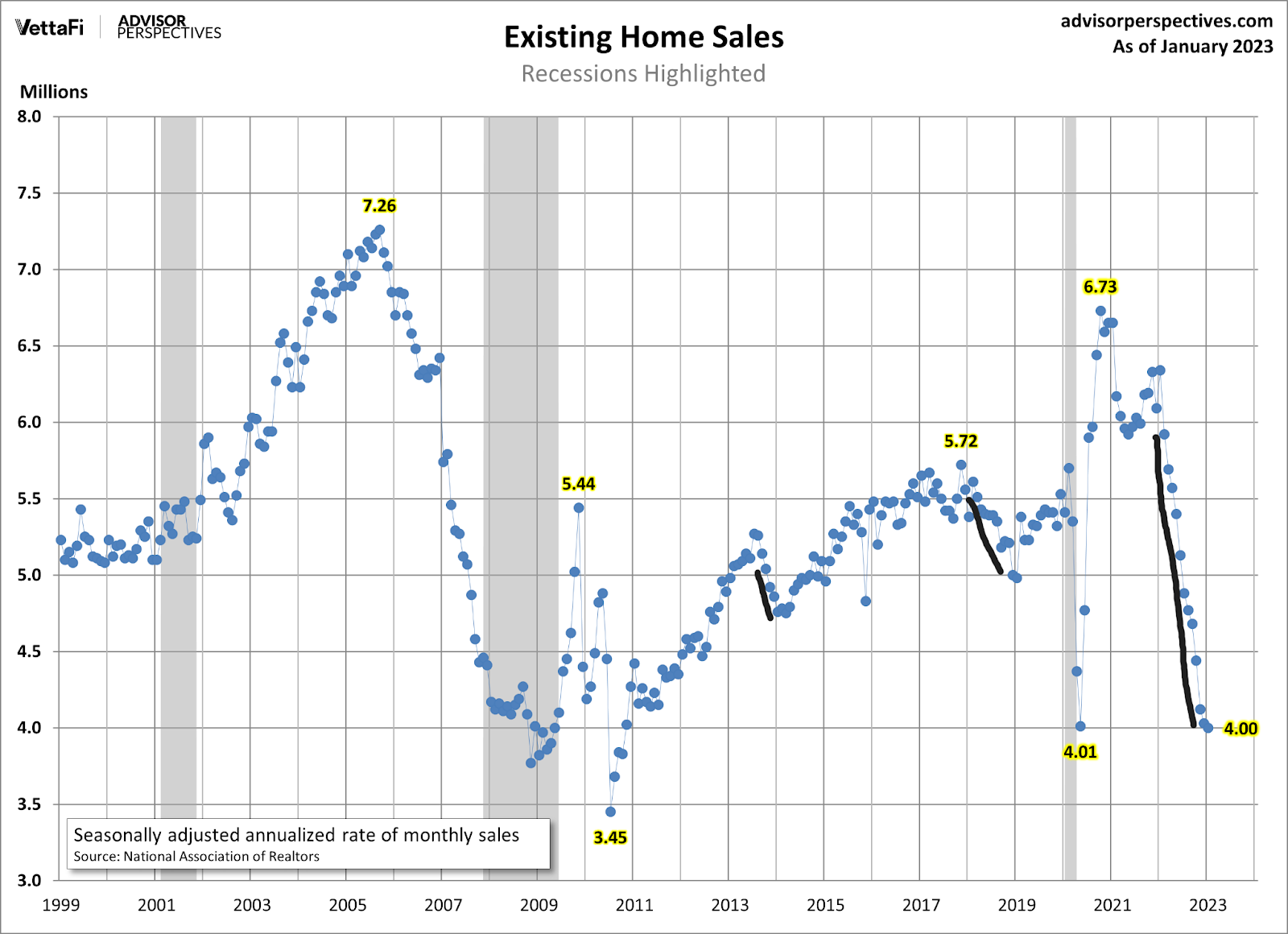

NAR Research: Very first-time prospective buyers have been accountable for 31% of gross sales in January Person investors obtained 16% of properties All-income revenue accounted for 29% of transactions Distressed profits represented 1% of product sales Homes usually remained on the marketplace for 33 days.

My problem for 2020-2024 has been that inventory degrees could crack to all-time lows, which indicates even if gross sales have been trending related to the earlier enlargement, we simply have far too quite a few persons chasing as well several residences. The bidding wars you listened to about this 12 months weren’t due to the fact of file-breaking desire but mainly because active listings are still close to all-time lows. The full inventory right now is however underneath 1 million at 980,000.

Stock is greater this yr than past, but I will soar for pleasure once again if we can just hit 1.52 million. This would give the housing industry a buffer in provide, just in circumstance property finance loan premiums drop once more. This did not happen this calendar year, so we hear tales of bidding wars once more early on in elements of the U.S. that do not have inventory in close proximity to 2019 concentrations.

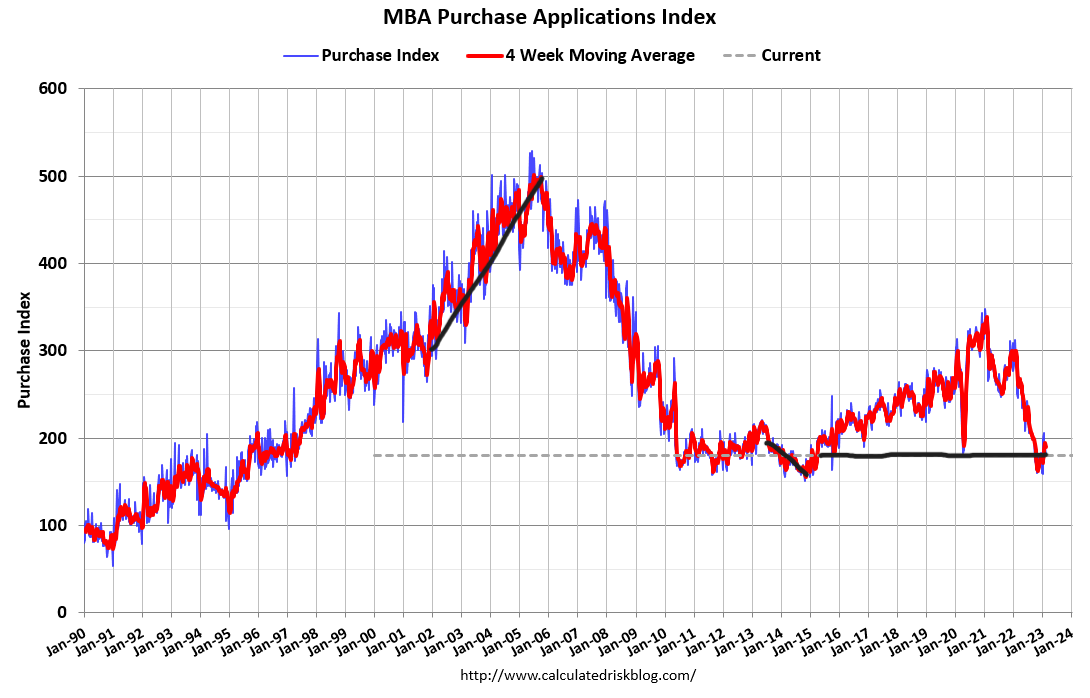

This is why previous week on CNBC, I cautioned persons to be mindful when speaking about housing booming once more. Forward-hunting purchase applications have risen from a waterfall dive, and we have noticed the data stabilize. We will bounce from this amount, but context issues.

This is why we designed the Housing Sector Tracker: data moves pretty quick, and now that mortgage fees have spiked up once again, we have to have to observe to see how significantly damage greater premiums do to demand from customers.

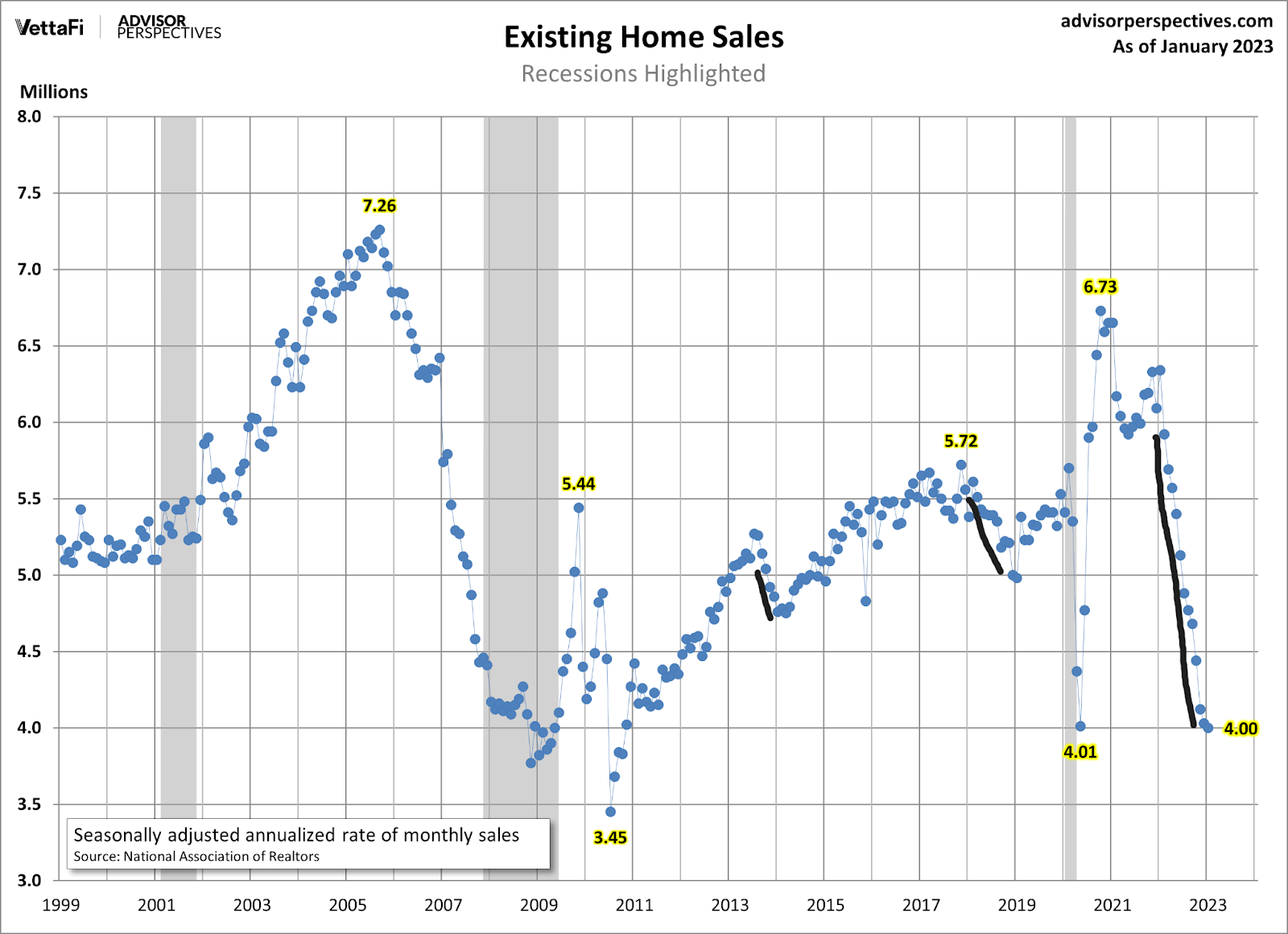

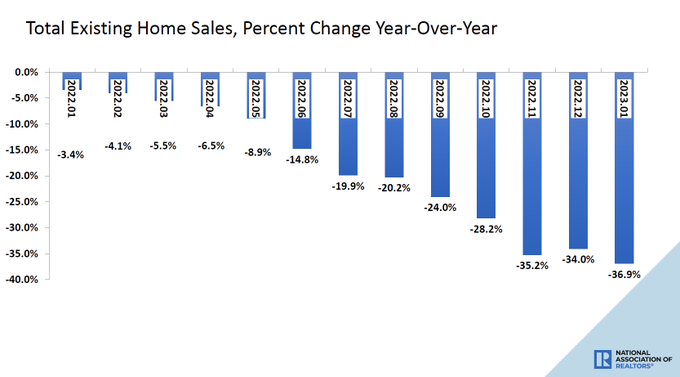

NAR: Complete current-home revenue: finished transactions that contain single-family members properties, townhomes, condominiums and co-ops, slid .7% from December 2022 to a seasonally adjusted annual level of 4.00 million in January. Calendar year-about-12 months, profits retreated 36.9% (down from 6.34 million in January 2022).

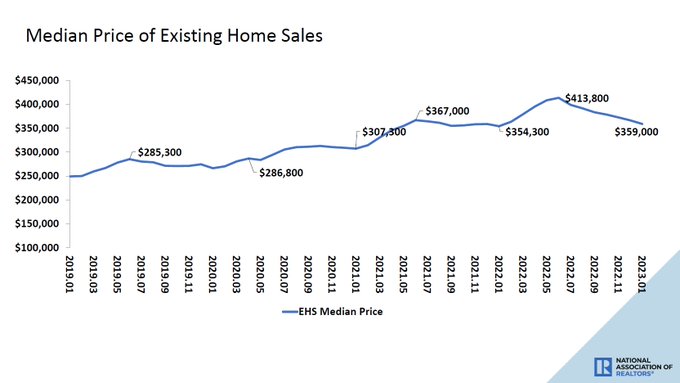

“Home profits are bottoming out,” claimed NAR Chief Economist Lawrence Yun. “Prices fluctuate based on a market’s affordability, with reduce-priced locations witnessing modest advancement and additional highly-priced areas experiencing declines.”

One of the ahead-seeking facts line details I have talked about because Nov. 9 is that housing need improved with purchase applications, so the worst product sales declines are in excess of. On the other hand, the profits details won’t demonstrate that enhancement right until February or March of this 12 months, which means the January and February present house sales reviews.

Purchase software knowledge is ahead-wanting 30-90 days, so it usually takes some time for better demand from customers to strike the existing home product sales report. However, it is very clear that the major major declines we noticed in profits in the 2nd 50 % of 2022 have settled down

Of study course, this implies we need to have to observe ahead-on the lookout knowledge, as better property finance loan charges need to sluggish the housing current market. The housing market can still be incredibly frustrating to potential buyers and sellers because mortgage costs can move speedy up or down. Considering the fact that the stop of June past 12 months, when charges went above 6%, new listing facts has declined, and this last week we strike a weekly new all-time small for the past 7 days.

- 2019 – 65,868

- 2020 – 62,447

- 2021 – 50,671

- 2022 – 49,159

- 2023 – 42,769

- This is not a very good tale for housing for the reason that a standard seller is commonly a standard consumer. So, if men and women don’t list their residences to provide and obtain, demand from customers can collapse, as we observed in 2022.

As you can see below, the calendar year-more than-yr declines are huge, but as the calendar year progresses, the declines should get a lot less if demand from customers is stable from these levels, primarily in the second fifty percent of 2023.

NAR Study: Calendar year-in excess of-year, gross sales retreated 36.9% (down from 6.34 million in January 2022).

Cost growth has cooled noticeably, in particular in the 2nd half of 2022. As someone who explained we necessary better costs in February of 2021 and deemed the housing current market savagely harmful in February 2022, this places a smile on my face.

NAR Investigate: The median present-residence cost for all housing types in January was $359,000, an increase of 1.3% from January 2022 ($354,300), as charges climbed in a few out of four U.S. areas although falling in the West.

My fear considering that 2020 has generally been that we would have important housing inflationary concerns if inventory broke to all-time lows all through 2020-2024. Of training course, this transpired, and then some, in the most destructive style at any time.

My rule of thumb for 2020-2024 was that if household costs grew 23% through these 5 several years, we would be ok with housing. This, of course, did not take place, as house charges grew 30% in just 2020-2021, and after premiums rose in 2022 soon after the important housing inflation strike, desire just collapsed.

Having said that, with that claimed, the 1 issue I wished to see to get again to a boring and well balanced current market at last occurred currently: days on the marketplace bought around 30 days.

This is a huge phase in having again to typical, even though I know my forecast past June of just finding complete housing inventory back again to 2019 ranges — which usually means just breaking around 1.52 million — appears to be negative now. However, a single of the variables for this to occur was to have days on the sector get above 30 times once more. This is a good phase in the appropriate direction.