The genuine estate sport is at a stalemate that reveals no symptoms of budging whenever before long, with neither purchasers nor sellers ready to make the very first transfer.

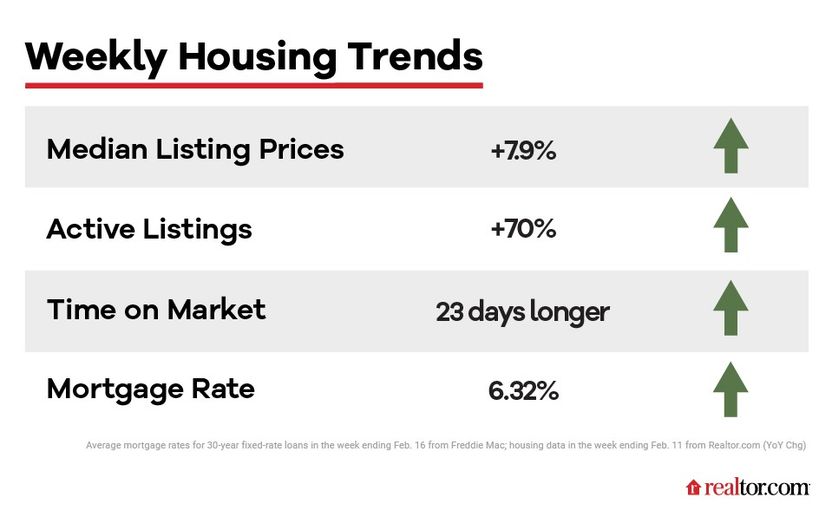

Consumers have very little incentive to guide the way. According to Freddie Mac, they are battling higher household rates and climbing house loan premiums, which rose to 6.32% for a 30-yr fastened-amount house loan in the 7 days ending Feb. 16.

In the meantime, property sellers—who, a mere calendar year before, appreciated packed open houses and bidding wars—are now battling to stand out from hordes of other sellers, as the pool of offered houses soared 70% higher for the 7 days ending Feb. 11 in contrast with the very same period of time final 12 months.

“The market’s abrupt adjustments over the past calendar year have produced it more durable for all participants to determine their possess boundaries, allow alone determine out how to meet up with in the middle so that a transaction can consider put,” states Real estate agent.com® Chief Economist Danielle Hale in her analysis of housing data for the 7 days ending Feb.11.

___

Enjoy: Property finance loan Costs Are Rebounding: What Takes place Future?

___

But amid the backdrop of soaring inventory and continue to-substantial property rates, yet another facts position indicates some sellers could be lastly eager to adjust up their strategy.

“January information demonstrates that the share of residence sellers building a value reduction was more than 2 times as big as one year in the past,” notes Hale. Indeed, 15.3% of sellers in January slashed their charges in comparison with 6% a 12 months earlier.

We will examine the most current genuine estate studies and describe what it signifies for homebuyers and sellers in this hottest installment of “How’s the Housing Market This Week?”

Why price tag cuts really do not always mean bargains

Irrespective of these price tag cuts, listing selling prices are however significant. In January, they clocked in at a median of $400,000, and they amplified by 7.9% for the week ending Feb. 11 compared with that similar week a calendar year earlier.

As well as, house loan prices remain around 2.5 percentage factors larger than last year.

This one-two punch of superior residence costs and house loan rates has sapped consumer motivation, adding to the current serious estate standstill.

“High residence prices and mortgage charges have essential spending budget contortions from buyers,” clarifies Hale.

Some property hunters have just offered up, permitting listings improve stale. For the week ending Feb. 11, households lingered on the market place 23 times extended than they did this exact same week a 12 months earlier. That’s the 29th week in a row that product sales have developed much more sluggish.

In fact, Hale notes the days a common house used on the sector in 2023 in contrast with 2022 has “grown sharply in recent months.”

Meanwhile, the dearth of sellers listing new houses continued its 32-week operate, with 13% fewer house owners listing their houses for the week ending Feb. 11 compared with this week previous year.

How purchasers and sellers should improve their strategies

So how do each buyers and sellers perform with each other to get the current market shifting once again?

“Both teams will want to adjust their expectations and be mindful of the slower marketplace tempo,” states Hale.

Funds-strapped potential buyers do have an abundance of a single point in the genuine estate recreation: negotiating ability. Those who seize this benefit could, instead than merely ignoring the industry, leverage this dynamic to snag a reduce home price to offset significant home finance loan fees.

Meanwhile, home sellers need to size up the glut of households on the market and, instead than cost large and trim that number later, rate their residences affordably suitable as they strike the many listing service—and capture a buyer’s eye from the get-go when their listing is contemporary and in need.

Hale also notes that today’s around comatose, tamped-down current market is not automatically a terrible detail.

“This slower current market speed is a return to what was ordinary just before the [COVID-19] pandemic,” Hale claims. “And consumers and sellers will will need to continue to keep this in head when getting into the housing market place this spring.”