Having said that, for 2023 I believe this selection on the 10-year produce would be acceptable, thinking about the labor market is nevertheless stable. If the labor current market begins to get worse — this means jobless claims increase with some pace — the original range of this forecast will crack, and bond yields will go lessen. The facts is not there nonetheless to even have that discussion.

From my 2023 housing industry forecast: “For 2023, the 10-yr generate is currently at 3.70% and I imagine the 10-12 months generate array this year will be amongst 3.21%-4.25% as lengthy as the economic system stays firm. Now if the economy will get weaker, particularly in phrases of the labor market place breaking, which for me is jobless statements climbing to 323,000 and beyond, then we can get as very low as 2.73% on the 10-yr produce.

“With that 10-calendar year generate assortment (3.21%-4.25%), home loan prices need to be between 5.25%-7.25%. This assumes that the spreads are extensive and pricing for mortgages is still weak. However, if the spreads get improved, we could even see property finance loan charges under 5% if the 10-calendar year generate breaks underneath 3%.”

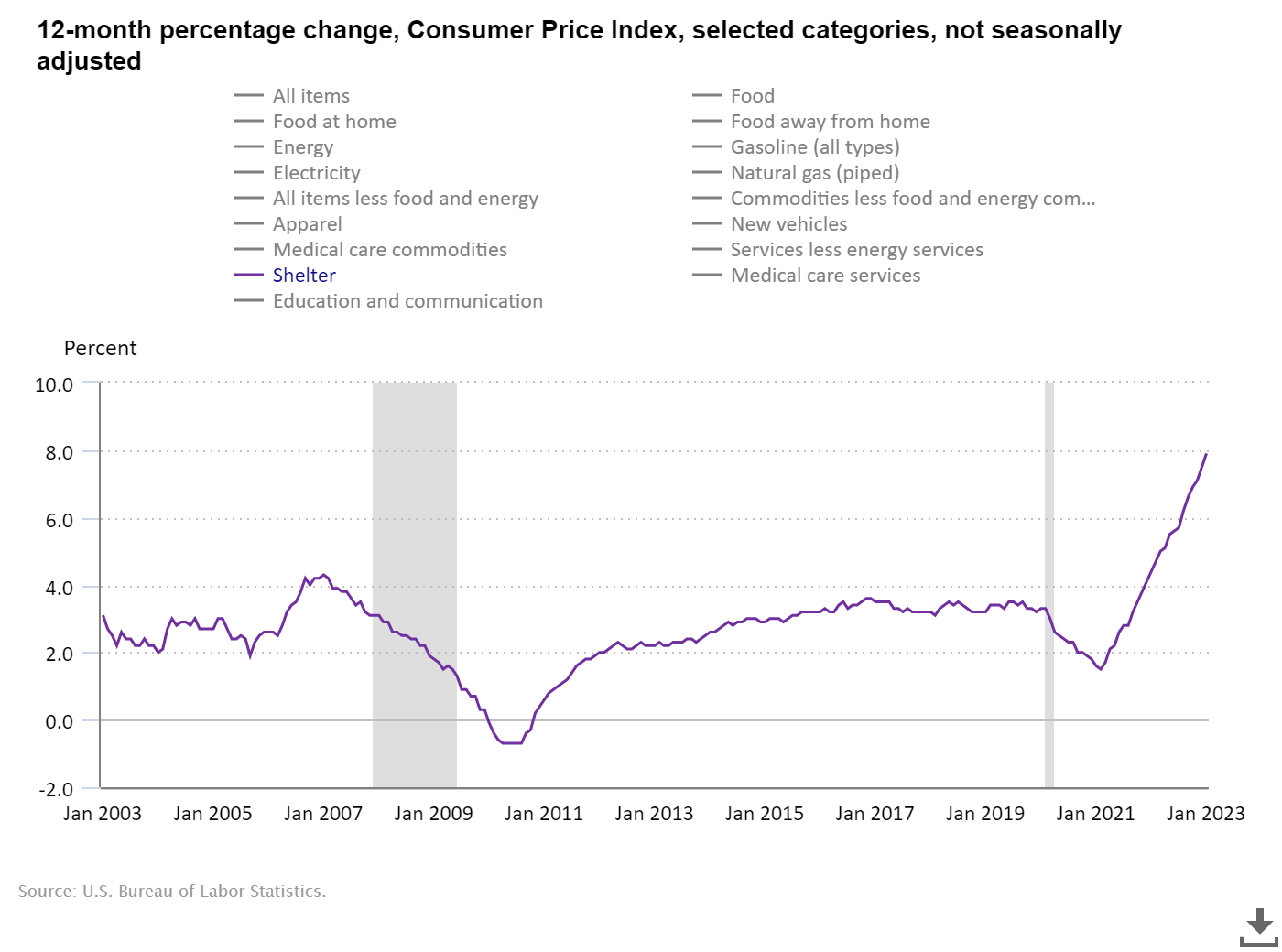

What do we know about inflation? The advancement amount is cooling from final year’s peak, and the shelter inflation portion of housing will neat down above time. It is widely regarded that the CPI inflation shelter data lags a great deal, and due to the fact it’s the most substantial ingredient of main inflation, it is a massive offer.

This is why I went on CNBC previous 12 months to say the progress price of rents falling was a positive for inflation for 2023. On the other hand, the CPI information lags badly on this fact, and the concern was that the Federal Reserve didn’t have an understanding of this.

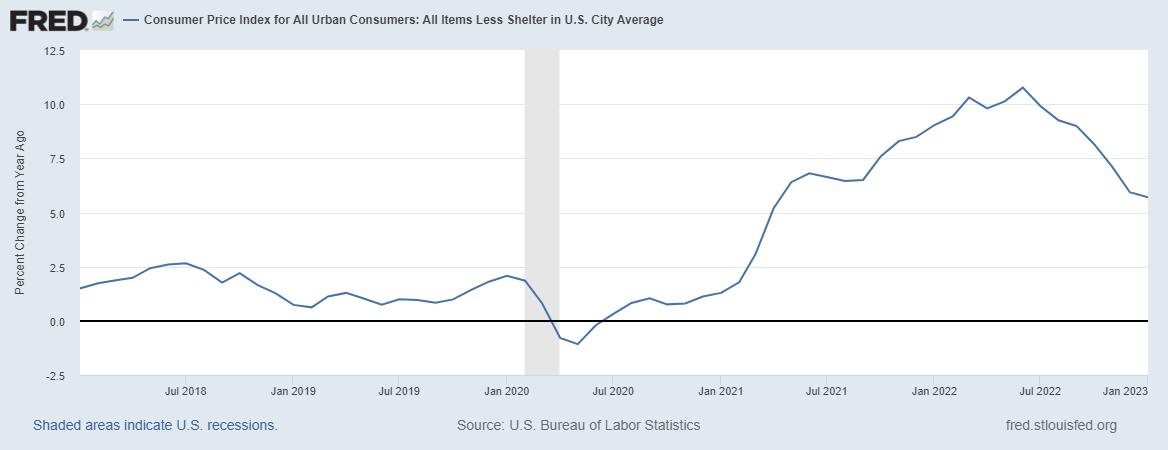

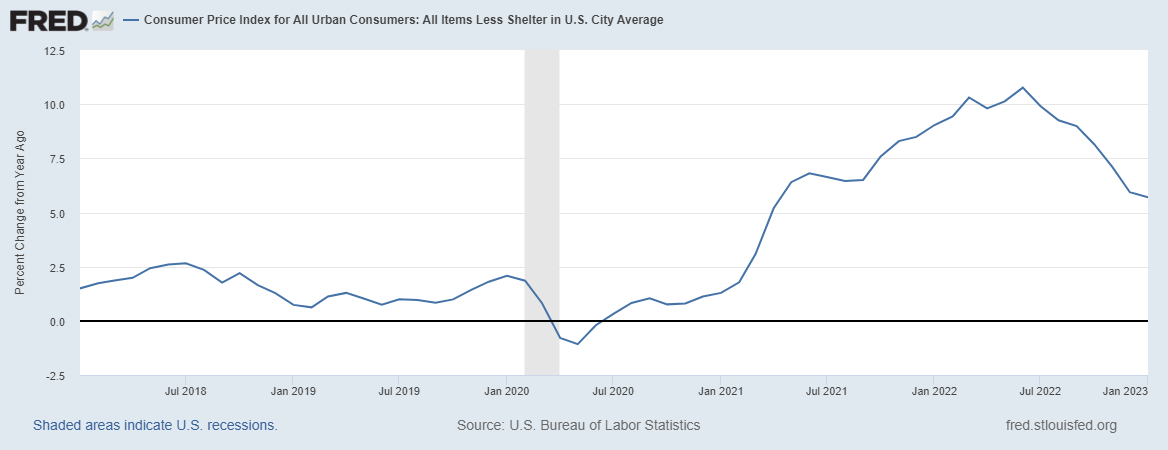

On the other hand, then the Federal Reserve essentially designed a new index that excludes shelter to adapt to the far more existing info, which exhibits the advancement fee of rents is cooling down. Now the Fed focuses on core inflation knowledge, excluding foods and electrical power. However, even if I consider shelter absent and leave food stuff and strength inflation in the equation, the development rate of inflation is cooling far more significantly.

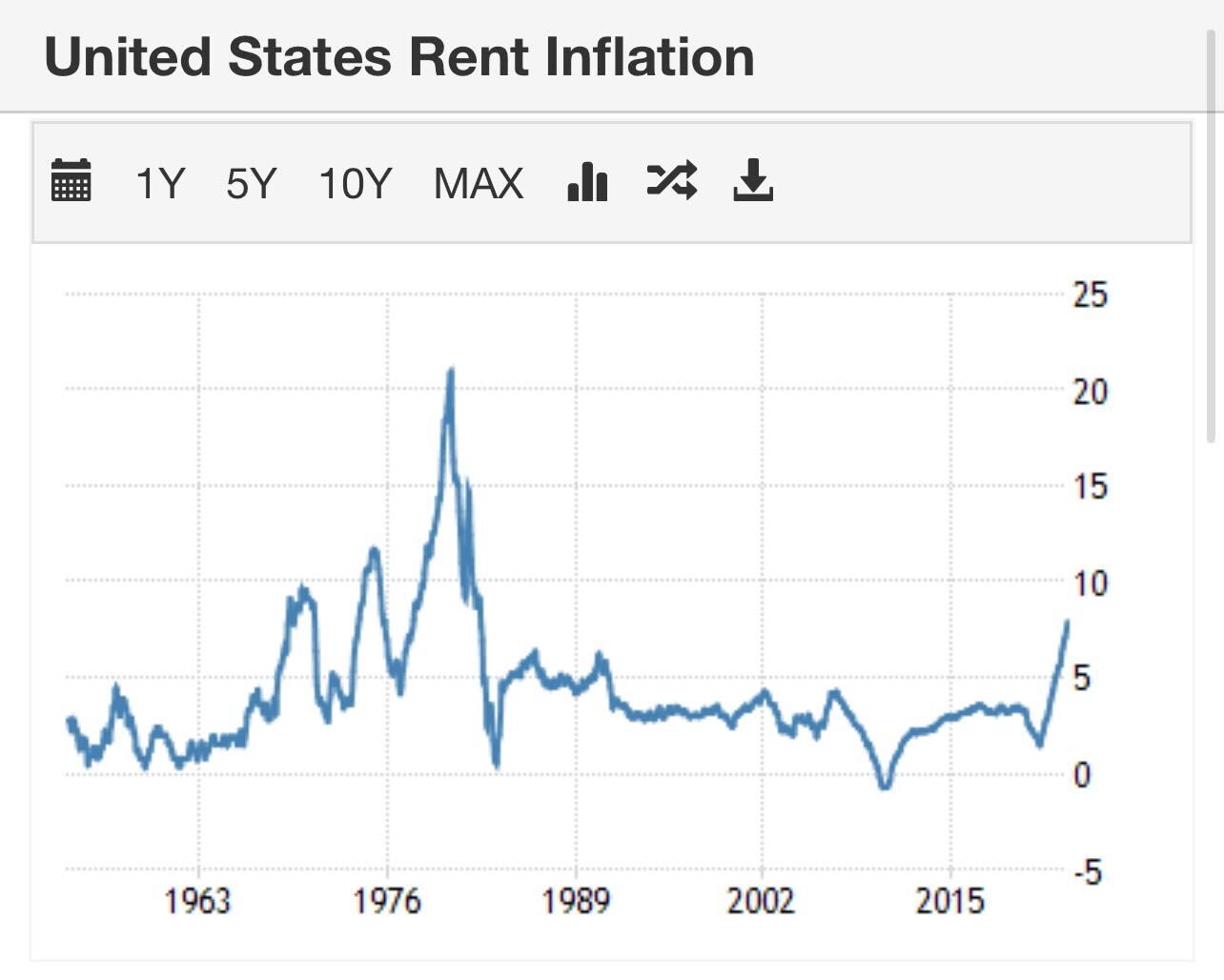

With no hire inflation taking off, you can kiss the 1970s inflation comparisons goodbye, and this is why the 10-12 months generate never broke earlier mentioned 5.25% — a important degree for me to even have a thought about 1970s-type inflation. As you can see under, the growth fee of rents took off a couple of occasions back then. Following the 1970s, the expansion level was secure for a long time.

My mentality with inflation information since Oct of 2022 has been to give it time: 12 months from now, we will be in a improved area. If the financial state went into a position-loss recession, the bond market would get effectively ahead of the Fed and home finance loan premiums would fall more rapidly. Having said that, we aren’t there nonetheless.

The Fed pivot won’t materialize till jobless claims split in excess of 323,000 on the four-7 days shifting regular, but the truth is the bond market is not outdated and sluggish they will head that way just before the Fed does.

CPI report

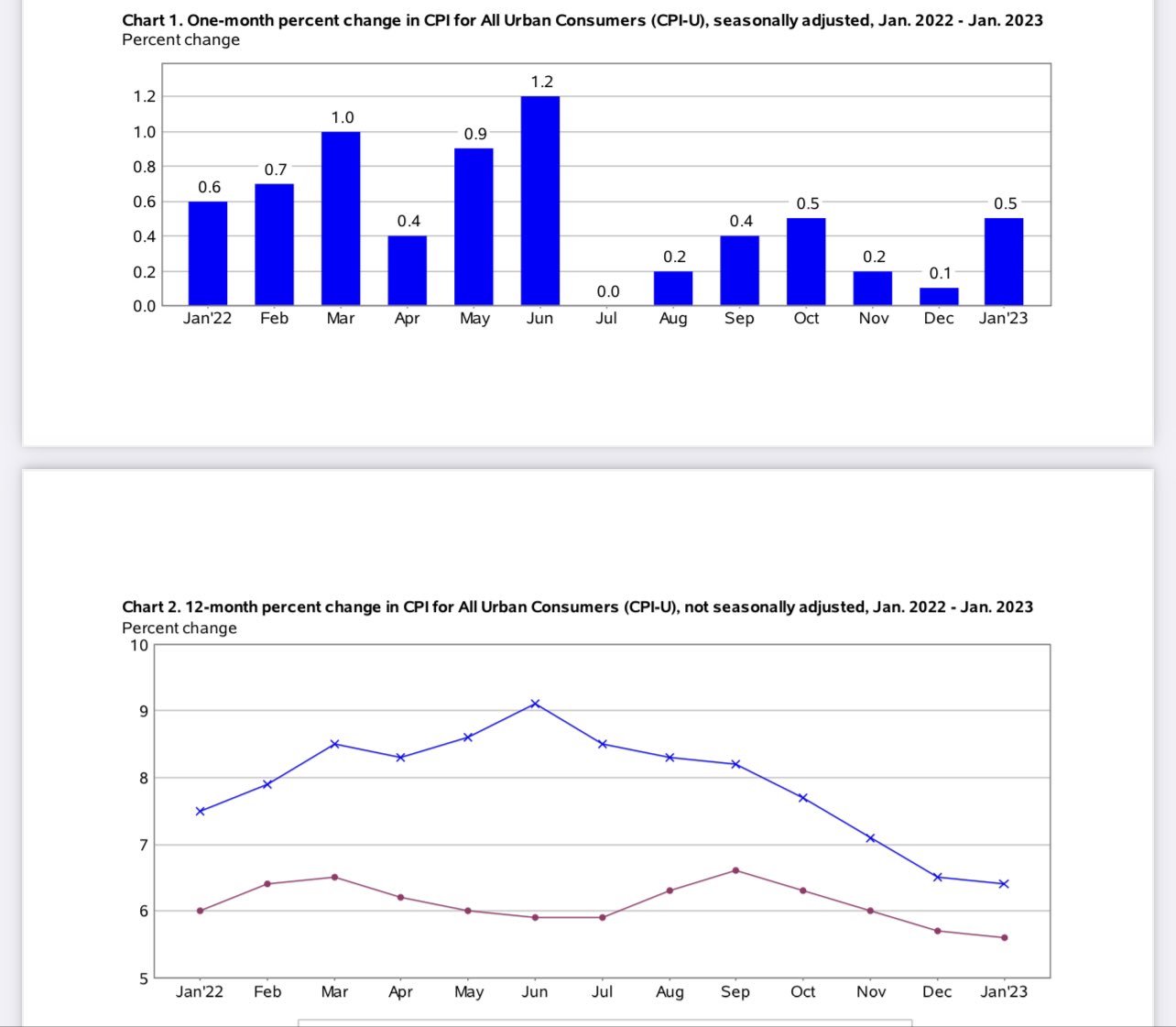

From BLS [bolding is mine]: “The Buyer Rate Index for All Urban Shoppers (CPI-U) rose .5 percent in January on a seasonally altered basis, following escalating .1 per cent in December, the U.S. Bureau of Labor Studies described these days. More than the final 12 months, the all items index amplified 6.4 % in advance of seasonal adjustment. The index for shelter was by significantly the biggest contributor to the month to month all things maximize, accounting for approximately 50 % of the monthly all objects boost, with the indexes for food stuff, gasoline, and all-natural gas also contributing.”

As we can see underneath, the growth rate of inflation is cooling, but shelter inflation, “Which is lagging authentic-time facts,” is maintaining the core info increased than it need to be nowadays. Remember, you need to normally aim 12 months out with inflation facts and tie it to the weekly financial data. This is why we made the weekly Housing Marketplace Tracker.

Other rental inflation knowledge shows a amazing-down, widespread with world pandemics. Even so, not only is the real-time knowledge cooling, we have nearly 1 million residences that will be constructed in the in the vicinity of long term, and the best way to deal with inflation is normally additional provide.

Ideally, this explanation of my forecast for 2023, such as the 10-year produce, home loan rates, and inflation gives you a greater being familiar with of why I don’t think home finance loan premiums can increase previously mentioned final year’s peak of 7.37%.

Now, a single way mortgage loan costs could blow past 7.37% is if the overall economy starts off to boom again, provide does not grow, and wage progress, which has been cooling, reverses, and explodes greater yet again.

If rents and wages took off greater yet again, some new war developed a lot more of a provide shock, and the labor current market bought even tighter, this would counter my discussion that the progress level of inflation has peaked. Nevertheless, so far, it does not seem like nearly anything I just talked about is going on, so give it additional time, and the inflation expansion fee will average.